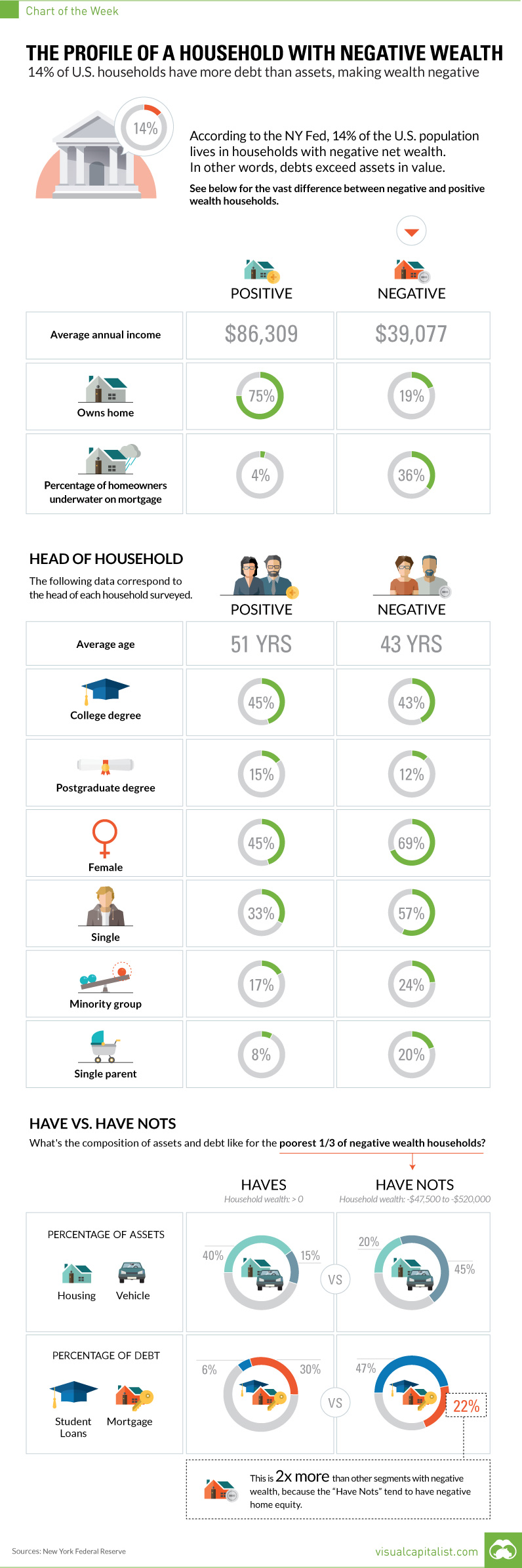

14% OF ALL U.S. HOUSEHOLDS HAVE MORE DEBTS THAN ASSETS

The Chart of the Week is a weekly Visual Capitalist feature on Fridays.

According to the New York Federal Reserve, 14% of the U.S. population lives in households that have “negative” wealth. In other words, these are households that have more debts piled up than assets, which puts their net worth in minus territory.

But what does a negative wealth household look like?

In today’s chart, we compare the data on negative wealth households with the data on their positive counterparts. There are some obvious and stark contrasts.

POSITIVE VS. NEGATIVE HOUSEHOLDS

At the household level, the differences are probably what you would expect.

Negative wealth households bring in $39,077 in annual income, and only 19% of these families own their home. More than one-third (36%) of these mortgages are underwater.

Meanwhile, positive wealth households bring in $86,309 in annual income, and 75% of the families own their home. Only 4% of the mortgages are underwater.

THE HEAD OF THE HOUSEHOLD

For each of these households, we have data on the person that is the head of the household, or the breadwinner for each family.

In terms of education, there isn’t a big difference between the heads of negative and positive wealth households. Both seem to be similarly accomplished in terms of achieving college degrees (43% vs. 45%) and postgraduate degrees (12% vs. 15%).

However, there are greater differences when it comes to demographic profiles.

Negative wealth households have heads that are younger (43 vs. 51 years old), female (69% vs. 45%), and single (57% vs. 33%). There is also a higher proportion of minorities (24% vs. 17%) and single parents (20% vs. 7%) living in negative wealth households.

THE HAVE AND HAVE NOTS

We also wanted to see the difference in composition of both assets and debts.

In this case, we are comparing the poorest third of those with negative wealth (-$47,500 to -$520,000) to those with positive wealth.

Households that are deep in the red have the majority of their wealth in the family car – automobiles make up 45% of the value of their total assets. Housing makes up 20% of their assets by value. For positive wealth households, it is the reverse: 40% of wealth is in the home, and 15% in vehicles.

The composition of debt is also very telling. Negative wealth households have a whopping 47% of debt in student loans, while positive houses have just 6%.

Source: http://www.visualcapitalist.com/14-percent-americans-negative-wealth/