Full size / "Based on this Sept 11 sat-photo the Grasberg open pit (one of the largest worldwide) has been flooded with a huge (mud) slide." (Willem Middelkoop on X.com on September 25, 205)

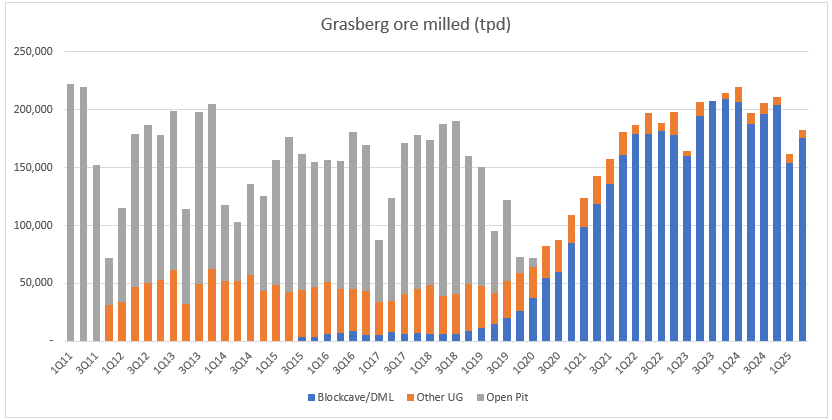

"Grasberg is a giant. One of the largest mines on earth... Think of it as a vast underground city: 28,000 employees, 250 km of tunnels across dozens of levels. Each year, 35–40 km of new tunnels are added – roughly the length of Switzerland’s Gotthard Base Tunnel (57 km), the world’s longest rail tunnel. At its heart lies the Grasberg Block Cave (GBC), which accounts for ~70% of reserves and output... On Sept 8, disaster struck: ~800,000 tons of wet material suddenly rushed in, flooding multiple underground levels. The mud hit GBC directly – the very core of Grasberg’s production. A catastrophic failure. How was this even possible? Block caving itself may become central to the story..." (Alexander Stahel on X.com on September 24, 2025)

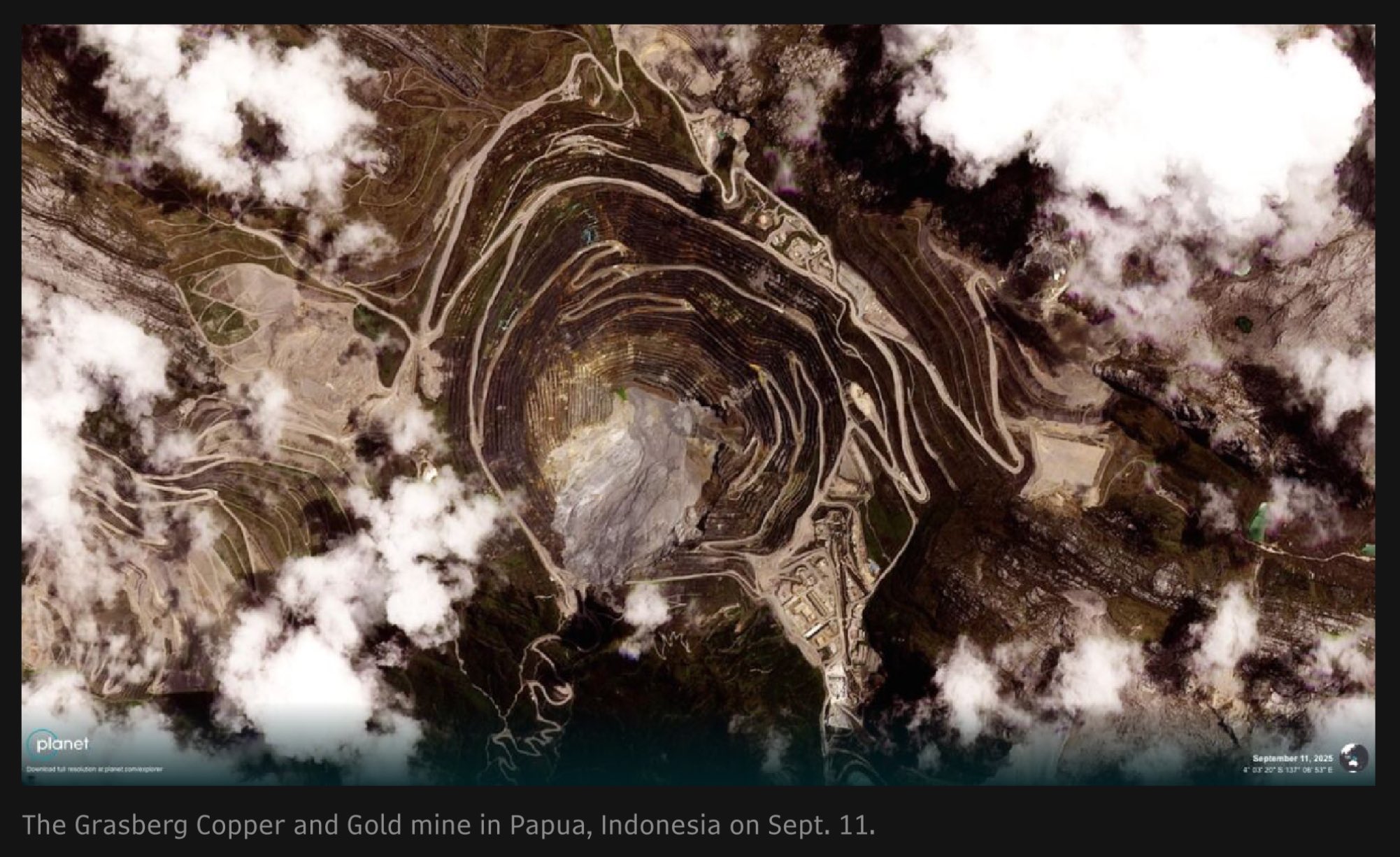

Full size / The Grasberg Copper-Gold Mine in Papua, Indonesia, is one of the world’s largest copper and gold mining operations. In production since the late 1980s, Grasberg has delivered more than 30 million t of copper and over 1,500 t of gold. The deposit, operated by Freeport-McMoRan in partnership with the Indonesian government, is renowned for its sheer scale, high-altitude location, and exceptional polymetallic endowment, with ore grades historically averaging around 1% copper and over 1 g/t gold.

"Out of more than 12,000 active mines worldwide, only ~20 have ever used block caving – a handful do so today - El Teniente in Chile; Oyu Tolgoi in the desert in Mongolia; Cadia East & Northparks, both Australia; Palabora, SA; who else? That’s <0.1% of all mines. None do so or did in the past within a similar rainy climate as Grasberg does. Block Caving is an extremely rarely applied mining method, reserved for very large, low-grade underground ore bodies which themselves are exceptionally rare. Most mining is open-pit, stoping, or cut-and-fill. Block Caving has economic appeal – low cost per ton – but the geotechnical risks are likely immense. Once caving starts, the process is essentially an engineered collapse of the mountain. What could possibly go wrong? That’s why this accident isn’t just a local disaster IMHO. It could become a case study for the entire mining method. Perhaps it wasn’t well understood how block caving behaves under Indonesia’s heavy rainfall and complex geology? I don’t know – but I wouldn’t be surprised if that proves decisive..." (Alexander Stahel on X.com on September 24, 2025)

"By year-end, Freeport will be fortunate just to understand the mechanics of this accident. Until then, production forecasts are pure guesswork. Such a failure should (a) have been impossible, and (b) means operations can only restart once it’s crystal clear why it happened and how it can be prevented from happening again. Analysts say full recovery is likely by 2027. That’s total nonsense. Nobody really knows... This is no quick fix. With infrastructure damaged, safety paramount, at least two confirmed dead and five still missing, investigations ongoing, potential class actions looming, and permitting hurdles ahead, the road back for Grasberg will be long and uncertain." (Alexander Stahel on X.com on September 24, 2025)

Full size / Source: Respeculator on X.com on September 24, 2025

Other Recent Copper Supply Disruptions

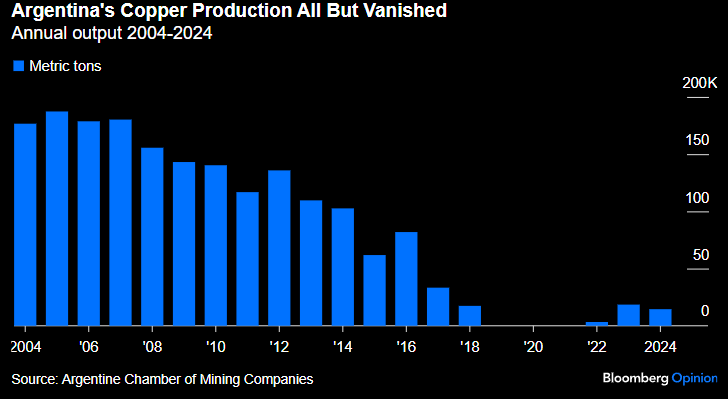

Full size / Argentina’s copper industry has all but disappeared over the past 2 decades, with annual production collapsing from over 180,000 t in the mid-2000s to near zero by 2024.

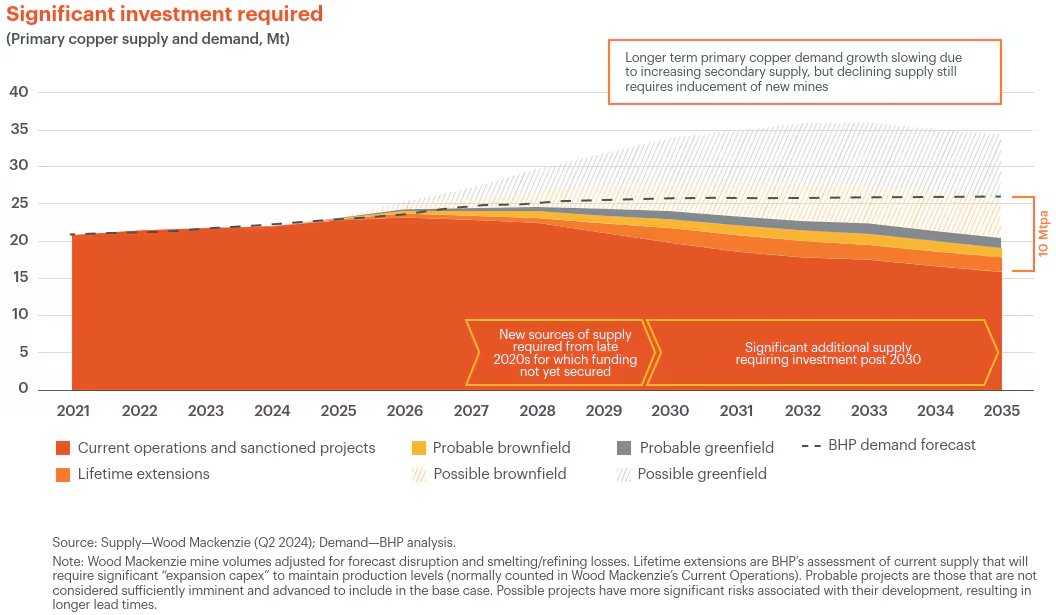

Full size / Supply analysis by Wood Mackenzie (Q2 2024); Demand analysis by BHP

Above chart highlights that even with lifetime extensions of existing mines and probable brownfield expansions, new sources of supply will need to be secured urgently. BHP’s demand forecast points to nearly 35 million t of copper needed annually by 2035, yet existing supply pipelines cover barely two-thirds of that requirement. This leaves a major investment gap in both greenfield and brownfield developments – projects that typically face long lead times, high capex, and rising regulatory hurdles.

This long-term picture dovetails with Goldman Sachs’ recent downgrade of global mine supply after the Grasberg outage. The forced shutdown at the Indonesian giant, which normally accounts for ~4% of global copper output, is expected to knock over 500,000 t of supply out of the market across 2025-2026, shifting the copper balance into deficit just as demand growth accelerates. Goldman now projects a 220,000–250,000 t deficit in 2025, with only a small surplus reappearing in 2026 if other mines deliver as planned.

“For years, copper bulls have talked up its key role in the transition to green energy, needed for wind turbines, electric cars and grid infrastructure. Now, the metal is riding two new megatrends: artificial intelligence and rising military spending. A proposed $53 billion merger between Anglo American and Teck Resources, the mining sector’s biggest deal for a decade, amounts to a giant play on future demand for the base metal. Copper consumption has been climbing for years but new supplies aren’t expected to keep pace with demand... The rise of artificial intelligence is powering a wave of extra demand for copper... “Significant amounts of copper are required to build, power and keep these centers cool,” said Anna Wiley, head of BHP’s South Australia copper business, at a conference last month. BHP, which sought to buy Anglo American last year to cement itself as the world’s biggest copper producer, forecasts a 70% increase in demand for the metal by 2050... All these factors are key reasons that help explain why copper has been at the heart of dealmaking in the mining sector in recent years – and why analysts say the proposed Anglo-Teck tie-up could spur rival offers as companies jostle for copper assets.“ (Excerpts from The Wall Street Journal‘s “Mining Megadeal Shows the World Is Crazy for Copper: Artificial intelligence and rising military spending are further buoying demand for the metal“ on September 10, 2025)

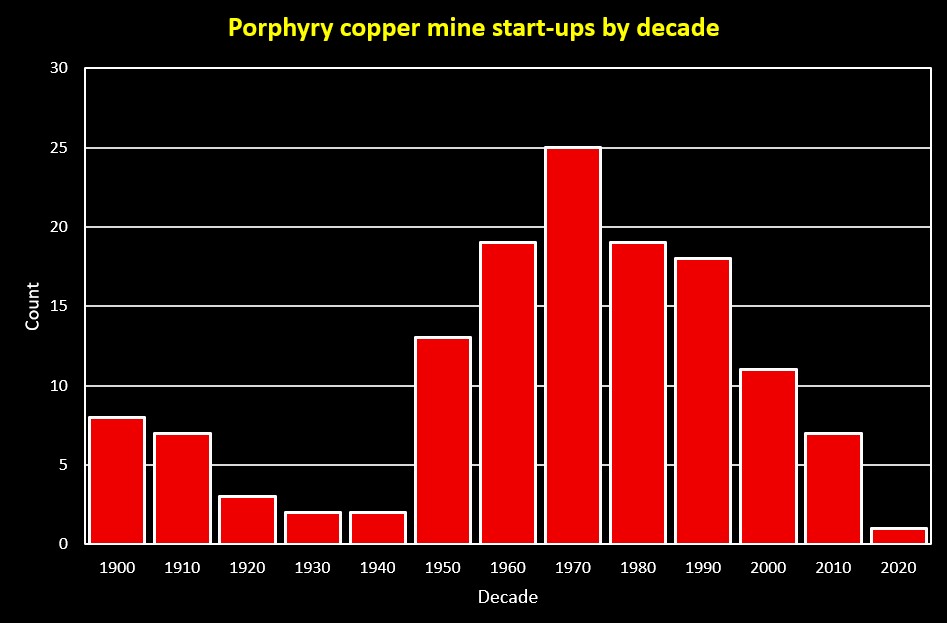

Full size / "The number of new porphyry copper mines in ten-year intervals- keep in mind that one of them from the 2010 decade was shut down a few years after it started (Panama). Remarkable that the LME warehouses have any copper inventory at all!" (J_Wise_geology on X.com on September 6, 2025)

The surge of new porphyry copper mines in the 1950-1970s coincided with rising global demand, robust exploration investment, and the development of large-scale open-pit mining methods. However, the sharp downturn in new start-ups from the 1990s onward reflects several converging factors:

• Maturity of discoveries: Many of the world’s largest and most easily developed porphyry systems were already discovered and put into production, leaving fewer “low-hanging fruit” opportunities.

• Falling grades and rising costs: Average ore grades declined, while permitting, development, and capital costs increased, slowing the pace of new start-ups.

• Price volatility: Periods of low copper prices reduced the economic viability of new projects, particularly large-scale, capital-intensive porphyries.

• Shift toward expansions: Rather than building new mines, many companies have focused on expanding or extending the lives of existing operations.

Investor take-away: The long-term decline in new mine start-ups highlights the scarcity value of genuine new discoveries. With demand for copper, gold, and molybdenum set to rise in the coming decades, companies advancing porphyry projects today are positioned to deliver outsized value as supply constraints tighten. This tightening supply pipeline highlights the scarcity value of new discoveries and underscores the upside leverage for companies advancing new projects today.

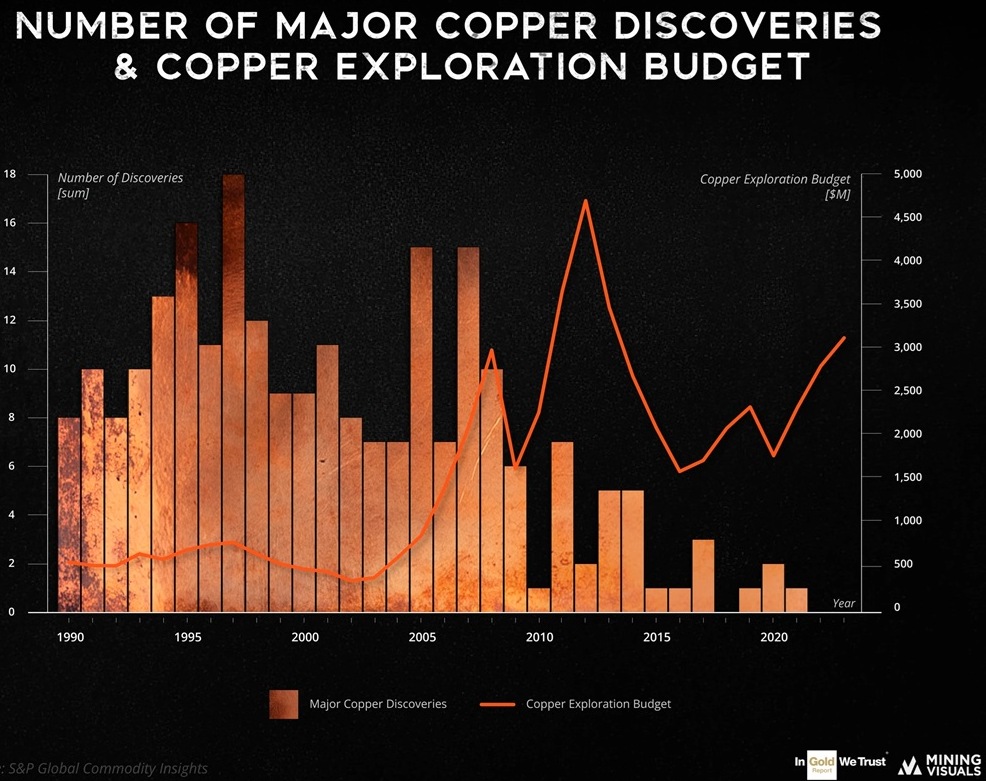

Full size / Source / Despite rising exploration budgets in recent years, major copper discoveries have dwindled to historic lows, underscoring the industry’s structural supply crisis. For investors, this shrinking discovery pipeline elevates the strategic value of high-quality exploration and development projects – particularly in stable jurisdictions –where genuine new finds represent a rare and highly sought-after addition to the global copper story.

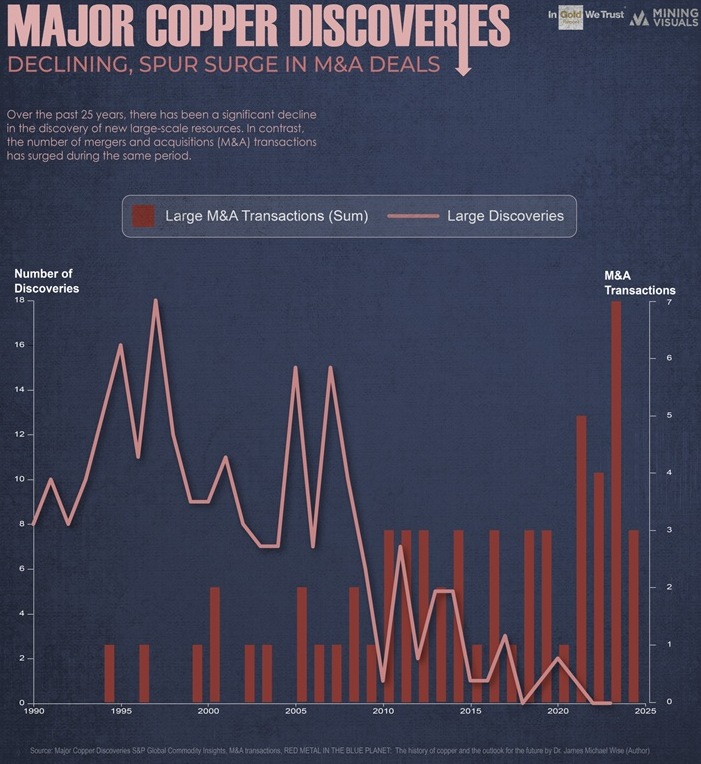

Full size / Source / Over the past 25 years, the discovery of new world-class copper deposits has fallen dramatically, even as industry exploration spending has surged. The chart illustrates how large discoveries have trended steadily downward, while mergers and acquisitions (M&A) have accelerated to fill the gap. With fewer genuine discoveries being made, major producers are increasingly forced to grow through consolidation, bidding up the value of existing assets.

For investors, this industry backdrop underscores a critical point: Organic discoveries are now exceptionally rare, highly strategic, and increasingly valuable. As global copper demand accelerates alongside electrification, energy transition, and infrastructure growth, the scarcity of new projects magnifies the importance of junior mining/exploration companies advancing fresh discoveries in stable jurisdictions.

Growing demand from AI-driven data centers, surging renewable power infrastructure, and rising global military spending further reinforce copper’s strategic role. Combined with accelerating EV adoption, grid expansion, and industrial modernization, the case for new discoveries has never been stronger or more urgent. In a market where majors are hungry for growth but short on organic discoveries, new deposits stand out as prime acquisition and partnership targets.

“Did you know that every time you type a query into ChatGPT, it requires about 10 times as much electricity to process as a Google search? That’s according to Goldman Sachs, which writes in a new report that electricity consumption in the U.S. is poised for a major surge for the first time in years, due in large part to the rapid buildout of data centers that power AI platforms such as ChatGPT... To help put things in perspective, ChatGPT currently has over 180 million users, but there are around 5.3 billion internet users around the world. Imagine if each of them became a regular user of energy-intensive ChatGPT, whose servers are located in the U.S., according to owner OpenAI. The U.S. is currently home to nearly 5,400 data centers, the most of any other nation by far. Even so, additional capacity will need to come online to meet runaway demand, and giant tech companies – from OpenAI and Microsoft to Google, Meta, Amazon and more – are spending billions to position themselves as leaders in the nascent industry... While natural gas will be a key player in meeting future power needs, copper is equally essential, particularly for its role in the energy transition. Copper is the only critical mineral present in AI as well as all of the most important clean energy technologies, including electric vehicles (EVs), solar photovoltaics (PV) and wind power. Its combination of conductivity, longevity, ductility and corrosion resistance makes it an indispensable mineral... However, the supply side of the copper market is fraught with challenges. To meet current trends, an astounding 115% more copper must be mined in the next 30 years than has been mined in human history.“ (Frank Holmes in "Data Centers Are Driving an Electricity Demand Surge from AI Platforms like ChatGPT" on June 3, 2024)

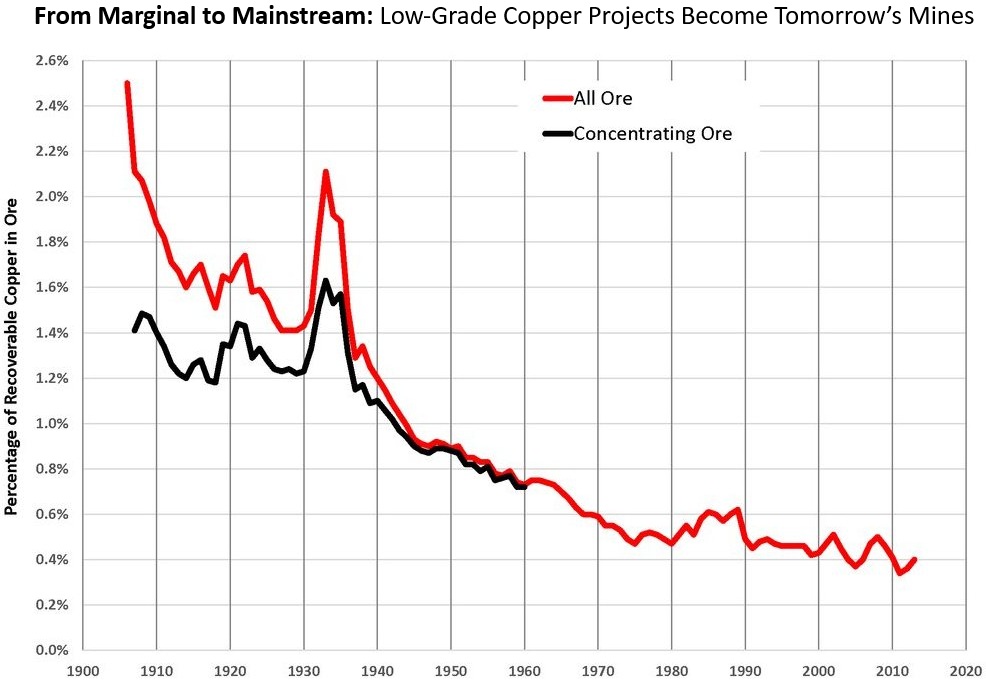

Lower Grades, Higher Stakes: The New Reality of Copper Supply

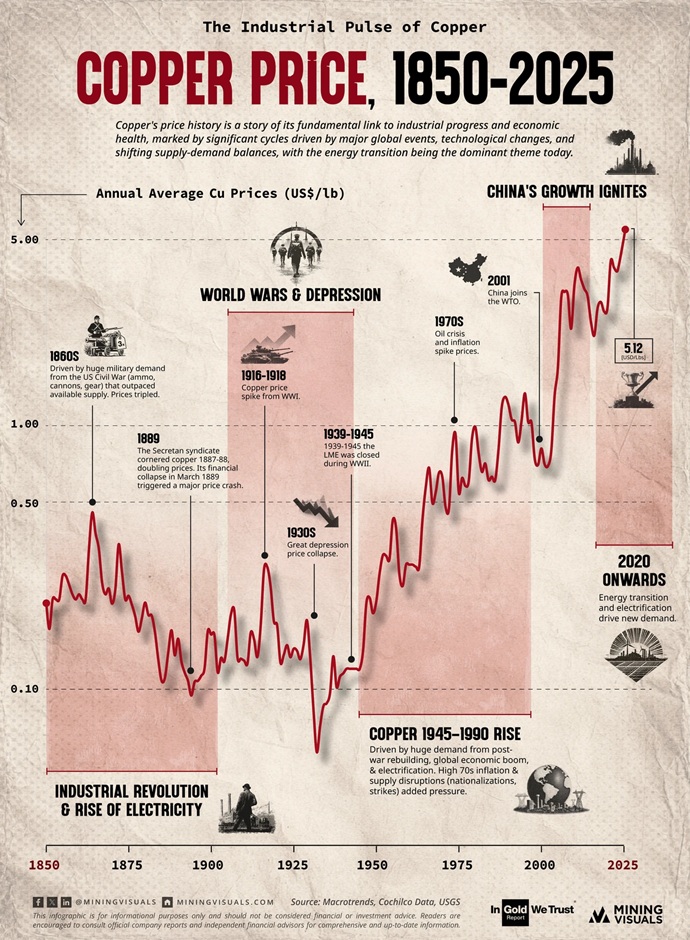

Full size / Often called “the metal with a PhD in Economics,” copper’s price has long mirrored the tides of industrial progress, global conflict, and technological revolution. From the telegraph wires of the 19th century to today’s data centers and EVs, every major shift in human history is etched into copper’s price curve.

• Industrial Revolution (1850s-1900s): Demand from electrification and war drove early spikes, with dramatic episodes like the 1880s Secrétan Syndicate attempting to corner the market.

• World Wars & Depression (1914-1945): Copper surged during war-time demand but collapsed in the Great Depression, with markets tightly controlled during WWII.

• Post-War Boom (1945-1990): Reconstruction, electrification, and industrial expansion fueled decades of steady growth, interrupted by the oil shocks and inflation of the 1970s.

• China’s Rise (2001 onwards): Entry into the WTO ignited the commodity supercycle, propelling copper into a new era of global demand dominance.

• The Green Transition (2020s): Today, copper underpins electrification, renewable energy, and digital infrastructure – driving structural demand that promises to shape the next supercycle.

Copper’s price history is more than economics – it is a chronicle of human progress. As the world accelerates toward a more electrified and sustainable future, copper remains at the heart of industrial and technological change.

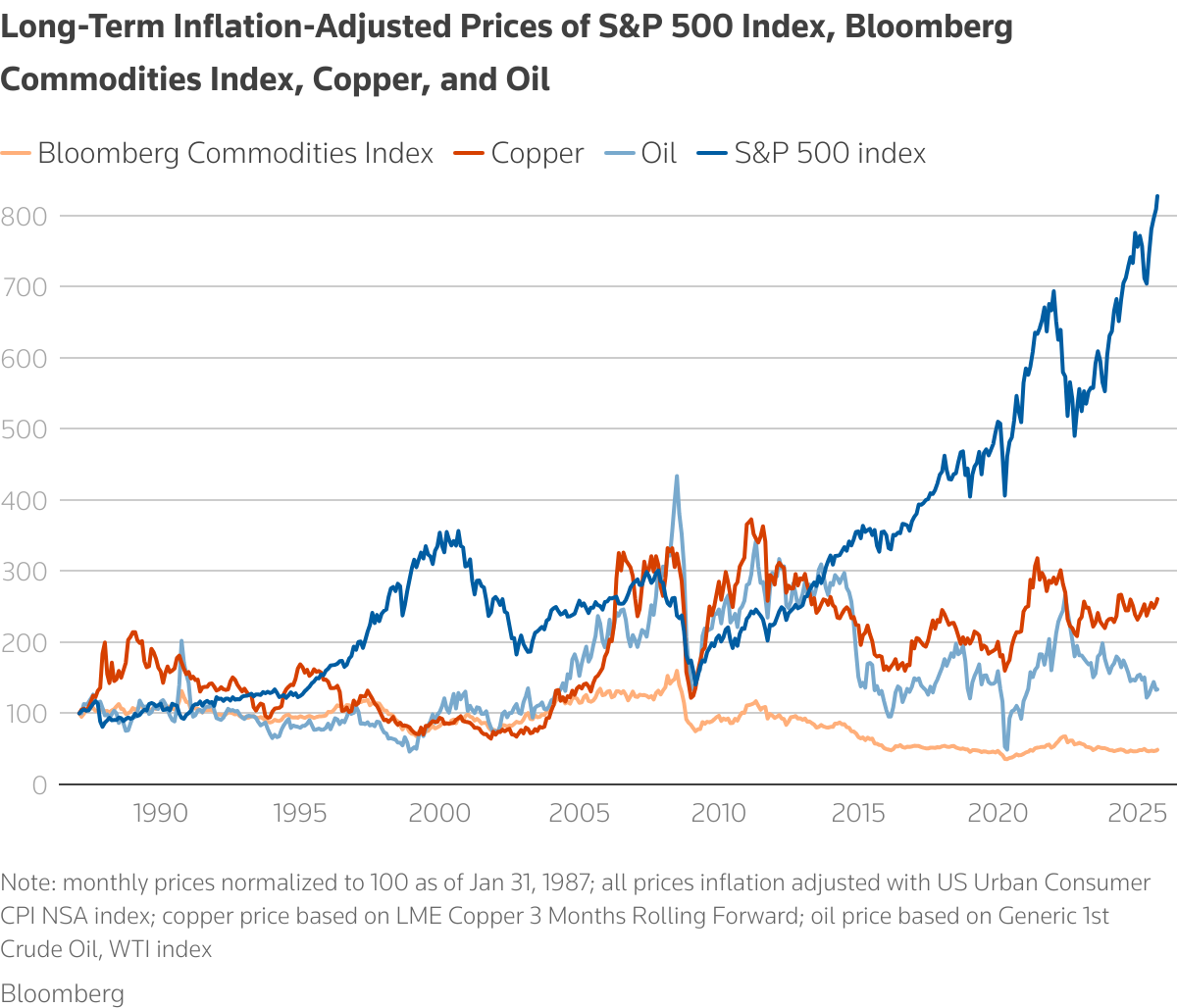

Full size / "Finally, the financial winds seem to be shifting in commodities´ favor. First, there’s the simple matter of price. The inflation-adjusted copper price remains 30% below its 2011 peak, while the inflation-adjusted oil price and the overall Bloomberg Commodities Index (which includes energy, industrial and precious metals, and agricultural produce) are 70% below their previous peaks in 2008. This is in stark contrast to U.S. equities where the S&P 500 index continues to hit all-time nominal highs and has almost tripled since its pre-Global Financial Crisis peak in 2007, even after adjusting for inflation." (Reuters in "Commodities could be on the verge of a new super cycle“ on September 18, 2025)

"Commodities have had a rough decade, but a confluence of structural factors suggests that after years of underinvestment, the stage may be set for the next super cycle. Commodities super cycles are long, powerful waves driven by major thematic shifts. The 1970s super cycle saw a mix of geopolitical supply shocks and loose monetary policy. The early 2000s super cycle was defined by China´s historic urbanisation boom. Today, there are structural factors on both the supply and demand sides of the commodities equation that could catalyze the next boom. To begin, the supply outlook for commodities overall has a few points of vulnerability that, if tested, could support a bullish long-term outlook. First, critical resources and the capacity to process them are highly concentrated in just a few jurisdictions. For instance, S&P Global reports that over 40% of the world´s copper production comes from Chile and Peru. Over 50% of the world’s iron ore is supplied by Australia and Brazil. And Kazakhstan alone accounts for over 40% of global uranium mine supply. This concentration extends beyond extraction to refining. China refines nearly 90% of the world´s rare earth elements, which are vital for everything from electric vehicles to defence systems. It also refines over 40% of the world’s copper, critical for AI and electrification. We have already seen examples of countries using their control of commodities supply as geopolitical leverage. China temporarily restricted rare earth exports in 2025 during trade disputes, and the U.S. included long-term Liquified Natural Gas (LNG) purchase commitments in its tariff agreements with the European Union and South Korea. This trend of weaving energy security and dependency into trade discussions and other geopolitical disputes creates a persistent risk premium that could erupt into severe supply disruptions down the line. Compounding this is a simple geological reality: the easy, high-grade deposits have likely already been found. Greenfield mining projects can now expect to face declining ore grades, soaring capital costs, and lead times that could exceed a decade. Years of underinvestment, partly due to shareholder pressure on miners to prioritise dividends over growth, have starved the pipeline of future supply." (Reuters in "Commodities could be on the verge of a new super cycle“ on September 18, 2025)

Full size / Source / Copper Futures Breaking Out: The chart of copper futures in USD per kilogram shows a decisive move above a 2-year downtrend (red line). After consolidating between $9.50 and $10.50/kg through much of 2023-2025, copper has now broken higher, signaling renewed bullish momentum. With structural demand from electrification and AI infrastructure colliding with fragile supply, this technical breakout reinforces the fundamental case for a sustained copper bull market.

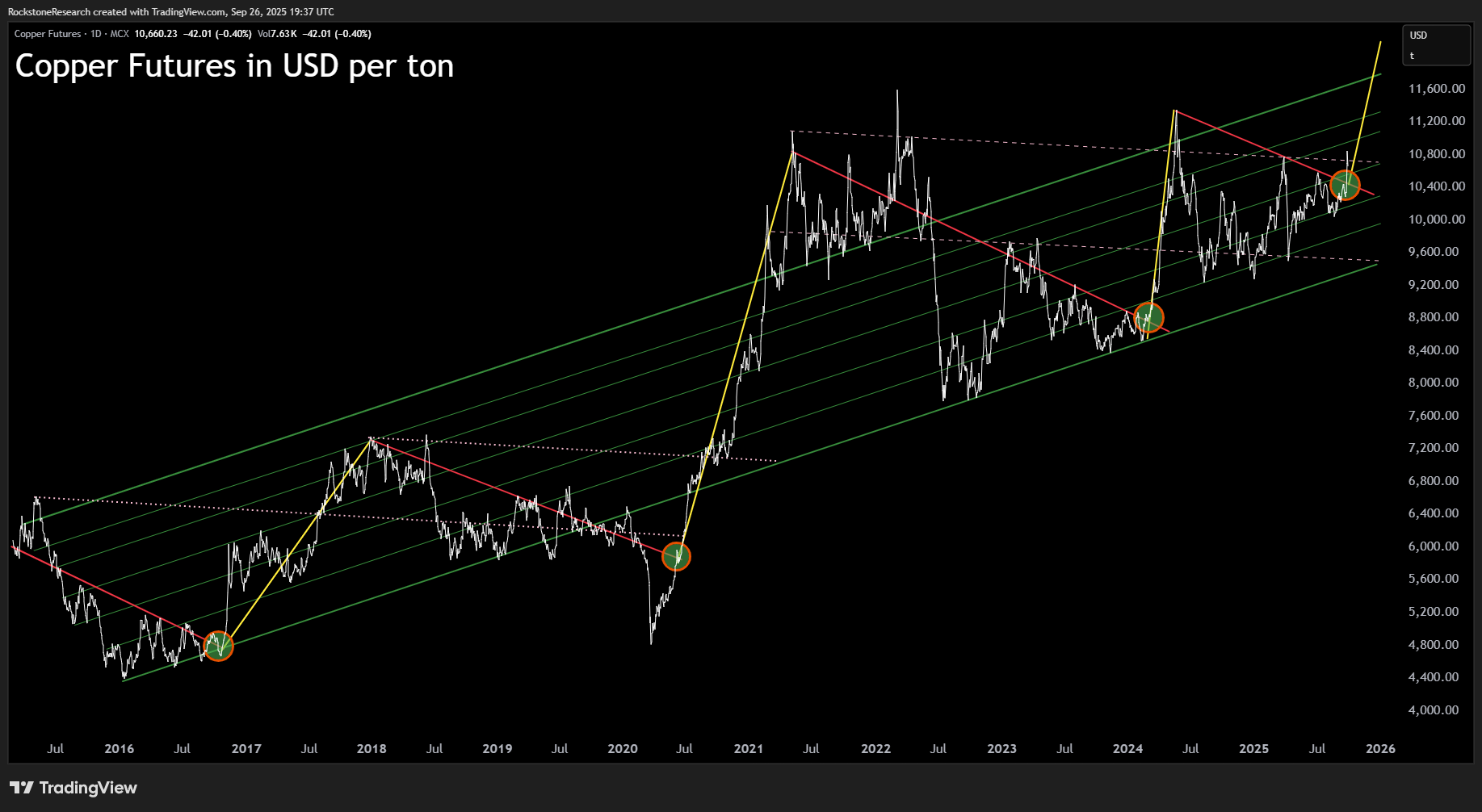

Full size / Source / Copper Futures in USD per Ton – Historical Breakouts Repeating: The chart highlights how copper consistently breaks major downtrends (red lines) with powerful rallies (yellow arrows), often triggered from long-term channel support (green). Each breakout has historically marked the start of a strong upside leg, as seen in 2017, 2020, and 2024. With the latest breakout now confirmed, copper is once again signaling the potential for a sharp move higher, targeting new highs above $11,000/t.

Bottom Line: Tomorrow’s Supply, Today’s Opportunity

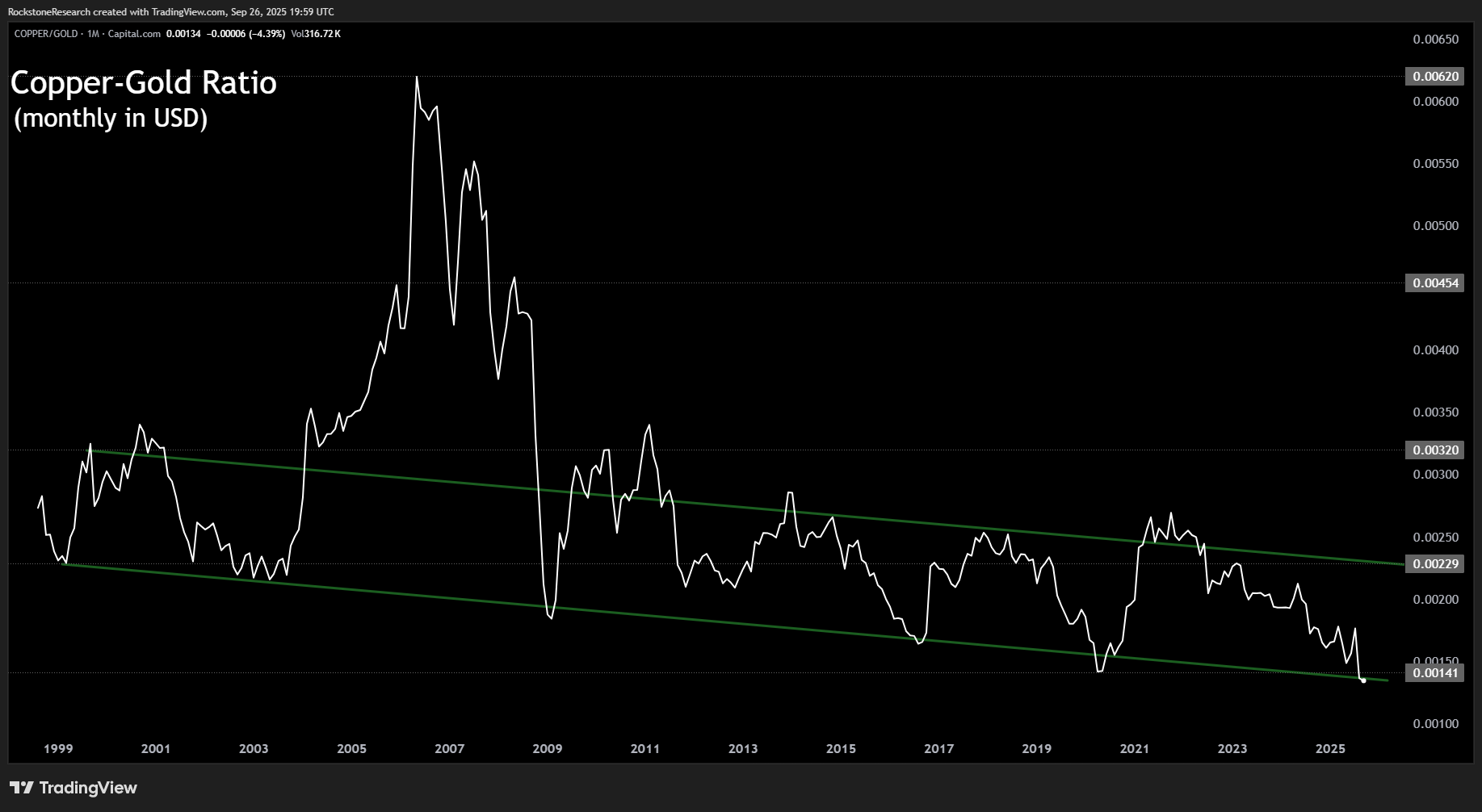

Full size / Source / Copper-Gold Ratio Near Historical Support: The long-term copper-gold price ratio has been in a steady downtrend since 2006, with each major low marking a turning point where copper began to outperform gold. The current reading (~0.0014) is testing the lower boundary of this multi-decade channel, suggesting a potential bottom may be near. For investors, this setup implies that copper could soon enter a period of relative strength versus gold, driven by structural demand while supply remains constrained. Historically, such lows in the ratio have preceded powerful copper rallies.

Full size / Source / Copper Miners ETF (NYSE:COPX) Breaking Higher: The chart shows copper miners surging to new highs, reflecting the powerful combination of rising copper prices and expanding margins across the sector. Large-cap producers have already delivered outsized returns, but the real asymmetric upside lies with copper exploration and development companies.

Unlike the diversified ETF basket of senior copper miners, the real opportunity lies with the juniors – exploration and development companies in stable jurisdictions which are steadily advancing high-quality projects. These are the names that majors turn to when they need to secure tomorrow’s supply.

And when consolidation comes, it rarely moves in half measures: Valuations can soar well beyond the broader market, delivering explosive upside that has historically outpaced both ETFs and established producers.

For investors willing to look one step ahead, this is where fortunes are made – not in tracking the herd, but in owning the very projects that will become the next generation of mines. In a tightening copper market defined by scarcity and strategic competition, today’s juniors are tomorrow’s headlines.

Contact:

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell commodities. The author holds physical gold and silver, stored in Central Switzerland through Elementum International AG. The author does not hold any direct interests or financial instruments related to other commodities or companies mentioned in this article. All views and forecasts reflect the state of knowledge at the time of publication and are subject to change. There is no guarantee that future developments will unfold as described. Investing in commodities involves risks. Consultation with a licensed financial advisor is strongly recommended. The cover picture has been obtained and licenced from Shutterstock.com