Disseminated on behalf of Interra Copper Corp. and Zimtu Capital Corp.

The threshold of $15,000 USD per ton seems to be the magic number for copper prices to incentivize new mine developments as supply is not keeping up with the strong demand growth. Back in 2021, Goldman Sachs said that copper is “on a necessary path to $15,000“ and “the most probable path for copper price from here – that both avoids depletion risk and as well as a sharp surplus swing – is to trend into the mid-teens by mid-decade“. Last month, billionaire mining magnate Robert Friedland reiterated that copper prices need to double to $15,000 USD to spur new copper supply. This month, CNBC reported on the optimistic forecasts of analysts from BMI, Bank of America and Citibank, with the latter projecting that copper prices could soar to $15,000 by next year. Such a dramatic price escalation could be akin to rocket fuel for pure-play copper exploration stocks.

Interra Copper Corp. is strategically positioning its shareholders with direct exposure to the anticipated copper bull market through a dynamic portfolio of copper porphyry assets in Canada‘s hot-spot regions of British Columbia, along with projects in Chile acquired from leading mining companies thanks to its well-connected management team with an impressive track-record of discovery and mine development.

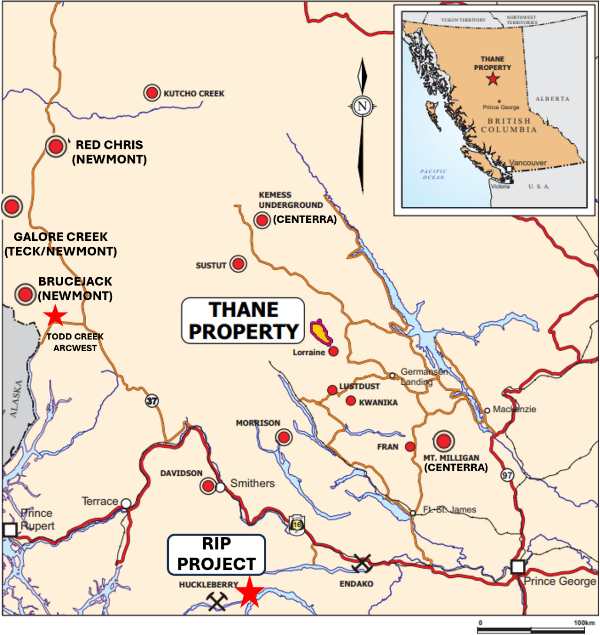

Having raised some $1.3 million recently, the tightly structured company (currently less than 29 million shares issued) plans to advance its newly acquired Rip Project. Interra also aims to further advance technical and exploration work at its other copper porphyry asset in British Columbia, the Thane Project. Both projects are surrounded by past producing mines and successful exploration activities from the majors.

“Build your new house out of copper bricks, cover the copper with gypsum wallboard so you forget it’s in the walls. Ten years from now you’ll be able to tear down the house and buy a fleet of electric Lamborghinis with your profits.” (Robert Friedland)

Copper Exploration vs. Copper Castle: Investing in copper exploration companies is like betting on the treasure hunters, while building a house out of copper bricks is like trying to live in the treasure chest itself.

Regulatory Riddles: Copper exploration and mining companies deal with regulations, sure. But try getting a permit for a copper house. “Yes, Mr. Inspector, the walls are metal. No, I‘m not building a giant microwave.“

Liquidity Laughs: Selling stocks in copper companies? Easy-peasy. In contrast, liquidating a house made of copper bricks would require dismantling and selling the copper, which is labor-intensive and might not fetch market prices. Selling your copper house? Picture trying to explain to potential buyers, “Yes, the walls are real copper. No, I‘m not a time-traveling alchemist. Yes, the WIFI is terrible.“

The copper industry is facing a critical situation as the supply is dwindling while the demand remains high, possibly leading to dramatic future shortages.

Aging Copper Mines: Most of the top copper mines are very old. The average age of the top 10 copper mines is about 95 years. This is significant because older mines typically have less production capacity and are closer to being depleted. A large number of copper mines are expected to stop production by 2035. This means that a substantial portion of the current supply will disappear in the next few years.

Lack of New Projects: Despite the rising copper prices, which usually encourages investment in new mining projects, there hasn‘t been a corresponding increase in the development of new copper mines. The situation is such that the number of new copper mining projects is not growing in response to the higher copper prices, which means that the price is still too low.

Stagnant Copper Resources: There‘s virtually no growth in new copper resources being discovered or developed. The chart shows that the increase in the amount of copper available for future mining is almost 0%. This indicates that not enough new sources of copper are being found to replace the old mines.

Impending Supply-Demand Issue: All these factors lead to a problem in the copper market. As the supply of copper from mines diminishes and no significant new sources are being added, we‘re heading towards a supply-demand crunch. Only higher copper prices appear to be the solution to stimulate exploration and development of new copper supply.

Full size / Source / “Where are we going to find the copper? Copper is already facing major supply challenges, including strikes, resource nationalism, global warming (droughts, water shortages), declining ore grades, depleted orebodies, a lack of new mines, and regulatory delays in building new ones. Moreover, the current copper price is too low to incentivize new mines... It is likely going to take a major out-of-stock event for the copper market to re-calibrate supply and demand with a price that both avoids depletion risk and a sharp surplus swing. Goldman Sachs forecasted in 2021 that the copper price (in tonnes) will reach the mid-teens by mid-decade. I’d say that’s on track. And it may not be a gradual uptick but a sudden increase. That will be an unpleasant surprise to end users...“ (Source: “A copper bug asks ‘who got copper’?“, December 2023)

Copper emerged as the top-performing industrial metal in 2023, maintaining its lead despite experiencing some setbacks in the latter half of the year. Looking ahead to 2024, market analysts anticipate a significant surge in copper prices, positioning this vibrant red metal to potentially surpass the performance of other commodities once more. This optimistic outlook acts as a powerful catalyst, fueling the momentum of stocks in the copper exploration sector.

Recently on January 2, CNBC noted in its article “Copper could skyrocket over 75% to record highs by 2025 – brace for deficits, analysts say“:

“Copper is headed for a price spurt over the next two years, as mining supply disruptions coincide with higher demand for the metal... Rising demand driven by the green energy transition and a likely decline in the U.S. dollar in the second half of 2024 will push copper prices higher, according to a report by BMI, a Fitch Solutions research unit... In a December [Citibank] report, the investment bank forecast that the higher renewable energy targets would boost copper demand by extra 4.2 million tons by 2030. This would potentially push copper prices to $15,000 a ton in 2025, the report added... Other analysts see a bullish run for copper due to mining disruptions, with Goldman Sachs expecting a deficit of over half a million tons in 2024... The winners of the copper rush will be mainly Chile and Peru, BMI estimates.“

Last December, billionaire mining magnate Robert Friedland said in a Bloomberg interview that copper prices need to nearly double to $15,000 USD/t to prompt mining companies to build new mines to meet the rising demand. Last summer, Friedland warned of a “copper train wreck“ if supply won‘t keep up with demand, stating that copper prices could jump 10-fold. “When metals are required, the prices go crazy and nobody’s willing to sell them,” Friedland noted. “We’re heading into that sort of situation.”

Interra: Strong Copper Portfolio in Canada and Chile

After initiating coverage on Interra Copper Corp. last year, when the company‘s 3 copper porphyry projects in Chile (Tres Marias, Pitbull and Zenaida) were highlighted, a new copper porphyry project in Bristish Columbia (Canada) was acquired: The Rip Project.

Work on the Rip Property has started already late last year with 3D topography and satellite-aerial survey (drone orthophotography) of the entire property as well as soil sampling (results are pending). Further exploration work is planned, consisting of geophysics to refine targets for the first stage of drilling.

Interra‘s Chairman and CEO, Rick Gittleman, commented in November 2023: “The execution on the Rip Project Option adds another promising project to the company’s portfolio and furthers our company’s objective of adding value through copper focused exploration and development. We look forward to working with our partners at ArcWest and unlocking Rip‘s potential.

Earlier in September, when Interra first announced its intent to option the Rip Project from ArcWest Exploration Inc., Interra‘s Director and COO, Jason Nickel, commented: “The Rip Project fits nicely into our portfolio of BC Copper properties, located in a high profile jurisdiction, and with nearby infrastructure and past producing mines. Partnering with ArcWest on the Initial work programs and our Phase 1 Earn-in, we look forward to uncovering what the present anomalies may discover.”

Tyler Ruks, President and CEO of ArcWest, added: ”ArcWest views the Rip Project as containing a highly underexplored porphyry copper system and is looking forward to working with Interra to advance the project.”

A large historically delineated IP chargeability high with areas of alteration, as defined from percussion drilling logs, a diamond drill hole, and outcrop, and the extent of strong quartz-sericite-pyrite alteration, provide for an immediate target area for exploration and future drilling at the Rip Project. Work at Interra‘s Thane Copper Porphyry Project in British Columbia is also planned.

Interra to Advance Copper Porphyry Projects in a Thriving Mining Hotspot

The remarkable richness in base and precious metals found in northwestern British Columbia has attracted mining and exploration companies for over a hundred years.

A significant portion of this activity is concentrated in the Stikine terrane, spanning more than 1,500 km across the length of the province and varies from more than 300 km to less than 100 km in width. During the pioneer era, gold was the primary focus for explorers, but only a few mines were developed. The discovery rate picked up in the 1950s, driven by the introduction of helicopter-assisted exploration and the realization that the area had potential for large porphyry copper deposits similar to those mined in the United States and Chile. It was during this time that the Granduc Copper Mine was explored and developed, with operations running from 1964 to 1984 (“a fascinating chapter in the history of North American mining“).

Recent exploration and development efforts are being stimulated by investments in infrastructure, including the Northwest Transmission Line and run-of-river power projects.

The Stikine terrane is home to many highly productive former mines, as well as current and future mining projects. These include the new Red Chris Copper-Gold Mine (70% Newcrest Mining Ltd. as operator; 30% Imperial Metals Corp.) and the Brucejack Gold-Silver Mine (one of the world‘s highest grade operating gold mines owned by Newcrest after acquiring Pretium Resources Inc. in 2022 in a $2.8 billion deal), the permitted KSM Copper-Moly-Gold-Silver Porphyry Project (the world‘s largest undeveloped gold project owned by Seabridge Gold Inc.), along with numerous other promising exploration and development ventures.

Interra‘s newly acquired Rip Copper-Moly Porphyry Project is near the past producing Huckleberry Copper-Moly Porphyry Mine, which was put on care and maintenance in 2016, with the current operator (Imperial Metals Corp.) focussing on exploration to expand the 2016-resource (181 million t @ 0.32% copper and 0.01% moly at a 0.2% copper cut-off) and develop a mine restart plan.

Less than 10 km from the Huckleberry mill, Imperial Metals is actively exploring its Whiting Creek Porphyry Deposit, returning 52.6 m @ 0.45% copper and 1.29 g/t silver in September 2023 and 162.5 m @ 0.33% copper and 11.64 g/t silver from volcanic rocks in November 2023 (“important as the highest grades and the majority of production at the Huckleberry mine came from altered volcanic rocks“).

Imperial Metals, earning revenue from its 30% stake in the Red Chris Mine and its wholly-owned Mount Polley Copper-Gold Mine in south-central British Columbia, is channeling funds into resuming operations at the Huckleberry milling facility. A revival of mining activities could be advantageous for neighboring companies like Interra.

Interra not only plans to explore the fully permitted Rip Project this year but also holds its 100% owned Thane Copper-Gold-Silver Porphyry Project in a relatively unexplored portion of the porphyry-rich Quesnel Terrane, midway between the past producing open-pit Kemess Mine (now underground development project) and the active open-pit Mount Milligan Mine,(both copper-gold porphyry deposits are owned by Centerra Gold Inc.). Recently, the vicinity of the Thane Property has garnered significant interest following the announcements by NorthWest Copper Corp. of impressive results from its 2022 and 2023 drilling activities at the Kwanika-Stardust Copper-Gold Porphyry Deposit.

RIP

Target Deposit-Type: Copper-Molybdenum Porphyry

Stage: Intermediate-Stage Exploration

Ownership: On November 28, 2023, Interra announced to have executed an Option Agreement with ArcWest Exploration Inc. (TSX.V: AWX). Interra has obtained a 2-stage option to earn up to an 80% ownership interest over up to an 8-year period.

• In the 1st stage, Interra has the option to earn, over a 4-year staged work-schedule, a 60% beneficial ownership in the Rip Project by issuing 1,050,000 shares of Interra, completing geological and exploration expenditures of $2 million and paying $100,000 cash to ArcWest over a period 4 years and 3 months until December 31, 2027. Interra will issue 200,000 shares before December 4, 2023. $25,000 of exploration is required by December 31, 2023, or payment to ArcWest in lieu.

• The 2nd stage of the earn-in requires Interra to advance the project to Feasibility Study level in order to obtain an additional 20% for a total of 80% ownership within 4 years of completing the first tier earn-in or at the latest December 31, 2031. This 2nd stage of the option requires Interra funding exploration work to reach a Feasibility Study and paying ArcWest $250,000 per year. Possible extensions are granted to Interra for 3 additional years (until 2034 at the latest), by continuing $250,000 annual payment to ArcWest plus an additional $100,000 per year in addition to a minimum of $2 million of annual exploration during the extension period.

Size: 2,309 ha

Access: The fully permitted Rip Property is road accessible from either Houston or Burns Lake.

Location: British Columbia, Canada

Full size / Magmatic axes in the Skeena Arch. The Rip Copper-Molybdenum Porphyry Project is located in the Skeena Arch, a belt noted for Bulkley aged (Late Cretaceous) porphyries and epithermal gold-silver deposits, including past producers (Huckleberry, Silver Queen, Equity) and significant resources (Berg, Poplar, Seel/Ox).

• Located about 63 km south of Houston and 79 km southwest of Burns Lake in central British Columbia, a prolific mining region on Canada’s west coast.

• Situated in Stikine terrane in a prolific belt of Late Cretaceous (Bulkley Plutonic Suite) porphyry Cu-Mo deposits, which includes the Huckleberry Mine (Imperial Metals Corp.; TSX: III; current market capitalization: $405 million) 33 km to the southwest of Rip and presently on care and maintenance. In addition, the Bulkley porphyry belt includes the Whiting Creek Copper-Silver Porphyry Deposit (Imperial Metals Corp.; 9 km north of Huckleberry mill), the Seel and Ox Copper-Moly-Gold-Silver Porphyry Deposits (Surge Copper Corp.; TSX.V: SURG) adjacent to Huckleberry, and the Poplar Copper-Moly-Gold-Silver Porphyry Deposit (Universal Copper Ltd.; TSX.V: UNV) 35 km from Huckleberry.

Full size / Regional geology of the Rip Porphyry Project.

Geology: The Rip Project covers the central axis of a 15 x 6 km window of Early Jurassic Hazelton Group volcano-sedimentary rocks intruded by several small stocks of Late Cretaceous Bulkley Plutonic Suite porphyritic granodiorite. Faults bounding this block trend northwesterly and separate the Hazelton Group from surrounding blocks of younger (Late Cretaceous to Eocene) volcanics.

Past Exploration: The Rip target was initially advanced by Kennco Explorations between 1975 and 1981. Kennco completed an IP survey in 1975, delineating a significant chargeability high. Although Kennco stated “in the final analysis this area will require an extensive drilling program to determine whether a zone of economic mineralization exists within the sulfide system” (Dorval and Stevenson, 1976), it was tested only by a single, 294 m long drill hole (at -45 degree inclination) in 1975. The hole intersected intensely quartz-sericite-pyrite (QSP) altered andesite and quartz diorite to a depth of 115 m where the zone was cut off by a fault. The QSP altered zone above the fault averaged 0.07% Cu and 0.005% Mo over 70.3 m (35.3-105.6 m).

Full size / A large historically delineated IP chargeability high with areas of alteration, as defined from percussion drilling logs, a diamond drill hole, and outcrop, and the extent of strong quartz-sericite-pyrite (QSP) alteration, provide for an immediate target area for exploration and future drilling.

• The IP survey was extended in 1980, outlining the 0.8-1.5 x 2.2 km chargeability high, and 36 shallow percussion drill holes totaling 1,763 m were completed (11 of the holes failed to reach bedrock). Logging of drill cuttings from these percussion holes delineated a zone of QSP alteration approximately corresponding to the chargeability high. A multi-element analysis of the core cuttings from 26 of the percussion holes in 1981 outlined a central 0.5 x 1.5 km Cu-Mo anomaly coring a broad peripheral lead-zinc-arsenic-manganese anomaly, a geochemical zonation typical of porphyry copper systems.

• Although most of the Rip Property is covered by glacial deposits, near the core of the Kennco chargeability anomaly a small (50 x 100 m) area of outcrop and shallow trenches exposes strong multi-stage porphyry-style stockwork veining within altered Hazelton volcanics and feldspar-quartz porphyry. Early magnetite-chalcopyrite-pyrite ‘A‘ veins with white K-feldspar (or albite) halos are cut by later quartz-chalcopyite-pyrite-molybdenite ‘B‘ veins. Veining accompanies pervasive magnetite-biotite (potassic) alteration which is variably overprinted by quartz-sericite-pyrite (QSP). Multi-stage porphyry-style veining locally reaches strong stockwork density. Limited rock sampling of these outcrops in 2017-2018 (8 samples) returned 258-1490 ppm copper, 3-238 ppm molybdenum, 7-69 ppb gold, and 0.2-1.5 ppm silver. Deleterious elements occur at very low levels (e.g., zinc < 77 ppm, lead < 4 ppm, and arsenic < 5 ppm).

Full size / Potassic altered porphyry with early magnetite-biotite veins cut by quartz-chalcopyrite-molybdenite veins.

Full size / Hornfels with quartz sulfide stockwork.

Full size / Hornfels with quartz sulfide stockwork.

Full size / QSP altered porphyry with quartz sulfide veins.

Full size / Hornfels with patchy/vein biotite magnetite sulfides.

Full size / Intense stockwork to sheeted quartz sulfide veining in trench.

THANE

Target Deposit-Type: Copper-Gold-Silver Porphyry

Stage: Intermediate-Stage Exploration

Ownership: 100%, NSR: 1%

Size: 20,658 ha

Location: British Columbia, Canada

Full size / A 240kV power-line runs along the Kemess Mine Road, approximately 10 km east of the Thane Property.

• Located in a relatively unexplored portion of the northern Quesnel terrane, midway between the previously-operated open-pit Kemess Mine (now underground development project) and the current open-pit Mount Milligan Mine, both copper-gold porphyry deposits are owned by Centerra Gold Inc. (current market capitalization: $1.6 billion).

• The area has received much attention lately with NorthWest Copper Corp. (current market capitalization: $27 million) announcing strong results from 2023-drilling at

the Kwanika-Stardust Copper-Gold Porphyry Deposit, e.g. 399 m @ 1.01% CuEq including 23.4 m @ 2.51% CuEq (from 152 m) and 151 m @ 1.55 g/t gold (from 363 m) and 64 m @ 2.12% CuEq (from 375 m).

• Interra spent $3.1 million on exploration since acquiring the Thane Project in 2020, including property-wide geophysics and 2,783 m of drilling (12 holes) at Cathedral (see here and here), which is just one of 6 highly prospective mineralized areas identified to date on the property. Each of the 5 bulk-tonnage-style targets have all sampled copper and gold mineralization with up to 13.9% Cu and 77.8 g/t Au (silver vein system with historical assays averaging 746 g/t Ag).

• In addition to Cathedral, Interra completed mapping, IP surveying, rock and soil sampling at the Gail and Mat Areas. Numerous geophysical anomalies were identified, most of which remain to be drill tested as high-priority targets.

• At the Cathedral Area, rock sampling identified 5 copper-gold showings that include the Pinnacle, Cathedral, Cathedral South, Arc, and Gully Showings (see results below).

Full size / Mineralized chloritic shear zone at the Pinnacle Showing. The dashed yellow lines delineates 10cm southeast trending moderate southwest dipping quartz-calcite vein. The dashed red lines delineates arsenopyrite+pyrite within sinistral chlorite shear parallel to sulphide veins.

The Great Copper Rush

Excerpts from “The investment opportunity for copper“ (June 2023):

Copper is the wiring that connects the present to the future. Global demand for copper is expected to double by 2035 driven not only by traditional sources of demand such as construction and infrastructure, but also by the adoption of new technologies that support a transition to a low-carbon economy, including electric vehicles, solar panels, and wind turbines... As the world electrifies, urbanizes, and grows wealthier, demand for copper will be challenging to meet, potentially bolstering the price of the metal...

Just as copper tools helped ancient civilizations emerge from the Stone Age, copper wiring plays a critical role in the world’s transition to a low-carbon economy. Copper is used in electric vehicles (EVs) and power grids, as well as in traditional infrastructure such as telecom wiring, plumbing and HVAC. Consequently, there is a secular demand surge for copper – driven not just by a low-carbon transition, but also the megatrends of rapid urbanization and emerging global wealth. As the “metal of electrification,” copper connects the past and future – generating exciting potential opportunities for investors...

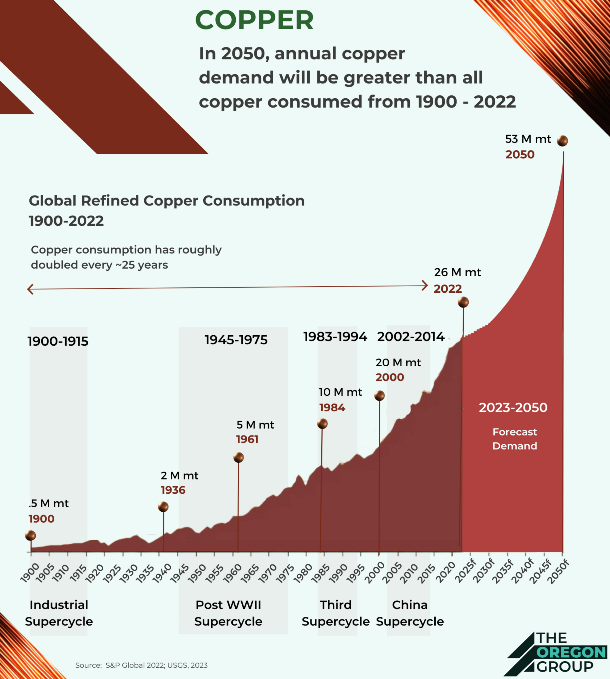

Demand for copper is forecast to grow from 25 million tons today to 53 million by 2050, driven by three key factors:

First, the electrification of transport, is projected to have the largest impact on copper demand. EVs require nearly 2.5x the amount of copper used in internal combustion engine (ICE) vehicles across electric motors, batteries, and charging infrastructure, and EV sales are projected to grow 35% in 2023.

Second, copper demand from power grids is projected to grow nearly 5x by 2050. Thanks to its unmatched conductivity and corrosion resistance, copper is used extensively in power distribution and transformers, particularly underground and subsea lines, and is needed to upgrade aging transmission infrastructure.

Third, the shift toward renewable power generation technologies such as solar and offshore wind – which require 2x and 5x more copper, respectively, per megawatt of capacity vs. gas and coal –should further increase demand.

In addition, the growing demand from building construction, appliances, electrical equipment, and cell phones, is still projected to account for 58% of copper usage by 2035.

As emerging markets continue to grow wealthier, and urban populations expand, copper is crucial to meet the demands of a growing middle class for electronics as well as the building needs of a rapidly urbanizing world...

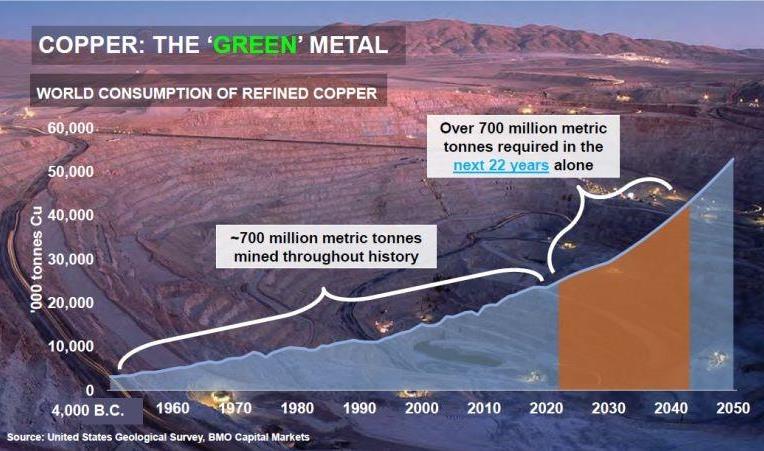

Copper – a soft, red-colored metal – is extracted alongside rock from copper-rich ore deposits in underground or open-pit mines. The world has approximately 870 million tons of untapped copper deposits. By the early 2030s, demand could outstrip the current supply by more than 6 million tons per year for two key reasons:

First, geographic concentration risk for copper production is high. Chile and Peru alone account for 40% of output. These countries possess some of the world’s richest copper reserves and best-established mining operations. However, political instability, labor disputes and economic challenges in the region periodically disrupt supply and lead to shortages and price fluctuations.

Second, existing copper mines are approaching production peaks. As high-grade ores become depleted, mining operations extract lower grades. Miners must now use grades of 0.5% copper (a measure of how much copper is present in rock) – a quarter the concentration of a century ago. As a result, more rock needs to be processed to extract the same amount of copper, raising extraction costs.

As a result of these constraints, global copper output in 2022 was 21.8 million tons, rising only 1 million tons over the previous three years and is expected to peak by the mid-2020s...

Management & Directors

DR. RICK GITTLEMAN

President, Interim CEO, Director

Rick is a legal, government relations and public affairs executive with over 35 years’ experience advising multinational companies on M&A, project finance, mining, oil and gas, agriculture and power projects across the globe. Most recently, he served as Senior Executive overseeing legal issues and stakeholder engagement at Glencore SA, where he developed corporate strategies to improve relations with government, community and civil society stakeholders at mine sites in Chile, Peru and Argentina. Preceding that, Rick held the position of Senior Vice President of Legal Affairs & Stakeholder Engagement at Freeport-McMoRan Africa, where over his 7-year tenure oversaw the Tenke Fungurume Mine in the Democratic Republic of Congo from development through to full commercial production. He also has 20 years’ experience as a partner at Akin Gump Strauss Hauer & Feld where he worked on merger, acquisitions and project finance in the energy and mining sectors. He served as a Peace Corps Volunteer in the DRC and graduated with a bachelor’s specialization in Political Science and American Civilization at Brown University and received his Juris Doctor (cum laude) from American University, Washington College of Law.

JASON NICKEL (P.Eng)

COO, Director

Jason is an experienced mining executive and engineer, investor and entrepreneur with a diverse 25-year mining background in operations, engineering, feasibility and exploration/development. Most recently, he held position as Mine Manager for a significant Canadian emerging gold producer, leading the production and development of new underground and pit operations. He has provided management and consulting services to the industry since 2008 and has been heavily involved with several junior resource public companies and mining project start-ups, mainly in British Columbia and the Arctic. He holds a degree in Mine Engineering from UBC and a GDBA in Business Administration from SFU Segal Graduate School of Business. Previously his experience includes several roles from Mine Planner, Senior Mine Engineer, Mine Foreman to Chief Engineer, Mine Manager and Vice President, primarily in copper and gold operations and projects.

PAUL ROBERTSON (CA, CPA)

CFO

Paul is the founding partner of Quantum Advisory LLP and has over 20 years of accounting, auditing, and tax experience. He has developed extensive experience in the mining sector and provides financial reporting, regulatory compliance, internal controls and taxation advisory services to a number of junior resource companies.

OSCAR OVIEDO (P.Geo)

Country Manager Chile

Oscar is an exploration geologist with over 20 years‘ experience in the exploration and discovery of copper deposits in Latin America. Previously, he worked as Project Geologist for Freeport McMoRan South America Ltda. in Chile, where Oscar was integral in the discovery of the Don Manuel Copper Deposit over his 13-year tenure. His work included a pivotal role in the initial exploration at the Tres Marias Project. Prior to that, he spent 7 years as Exploration Geologist at Minera Phelps Dodge of Peru SAC, discovering the Haquira Deposit. Oscar holds a degree in Engineering Geology from the National University of San Agustin in Peru.

MIKE CIRICILLO (B.Eng)

Director

Mike is a mining executive with almost 30 years of operational and project experience, having lived and worked on 5 continents. Mike began his career in 1991 at INCO Ltd. in Canada and later joined Phelps Dodge in 1995, which was acquired by Freeport-McMoRan, where he served in the US, Chile, the Netherlands, and the DRC. In the DRC, Mike was the President of Freeport McMoRan Africa and spent 5 years at the Tenke Fungurume Project (from construction into operations). In 2014, Mike joined Glencore as Head of Copper Operations in Peru, followed by the role of Head of Copper Smelting Operations, and eventually he served as Head of Glencore’s Worldwide Copper Assets.

DR. MARK CRUISE (P.Geo)

Director

Mark is an exploration and mining professional with over of 25 years’ global experience, having discovered, developed and operated mines in Europe, South America, Canada and Africa. He currently serves as CEO of New Pacific Metals Corp., having previously founded Trevali Mining Corp., where he grew the company from an initial discovery to a global leading zinc producer. He has held a variety of professional and executive positions with Anglo American PLC and various publicly listed exploration and development stage companies. Mark holds a Bachelor of Geology and a Doctorate of Geology from the University of Dublin, Trinity College. He is a professional member of the Institute of Geologists and the European Federation of Geologists.

RICK LEVEILLE (P.Geo)

Director

Rick has a lifetime‘s worth of experience in the mining sector, having grown up in major copper camps in the western US where his father worked for Kennecott. He has a B.S. Geology from the University of Utah and an M.S. in Geology at the University of Alaska, Fairbanks. He worked for a progression of companies including AMAX, Kennecott, Rio Tinto, Phelps Dodge and Freeport-McMoRan, where he was directly involved with and/or managed teams that made several major discoveries. His last corporate position was Senior VP Exploration for Freeport-McMoRan. He retired in 2017 and has devoted his time since then to hiking, backpacking, fishing, writing, advocacy for immigrants and geological consulting.

Advisors to the Board

DR THOMAS HAWKINS (P.Geo)

Technical Advisor

Thomas is a Qualified Person under National Instrument 43-101 as a Registered Professional Geologist (EGBC) who has nearly 20 years of international experience in identifying, assessing, and advancing exploration projects. In 2004, he graduated from Imperial College, London, with a Masters in Geology and Geophysics, and gained a PhD in Geology in 2012 from the Natural History Museum in the UK. Thomas has extensive experience in managing projects in Ghana, Mexico, Canada, USA, UK, and Kazakhstan. Most recently, Thomas was part of the Kenorland Minerals Ltd. team that discovered the Regnault Deposit and was VP Exploration of Northway Resources Corp. In 2018, as President of Vanmin Development Corp., Thomas discovered the Vanadium Pass Deposit in British Columbia.

DAVID GAROFALO (FCPA, FCA)

Special Advisor

David is an accomplished mining executive with 30 years’ experience in the creation and growth of multi-billion-dollar mining businesses across multiple continents. He is currently Chairman and CEO of Gold Royalty Corp, Chairman of Great Panther Mining Ltd., and Chairman and CEO of the Marshall Precious Metals Fund. Formerly, he was the President and CEO of Goldcorp Inc., a position he held from 2016 until its sale to Newmont Corp. in 2019. Prior to Goldcorp, he was President, CEO and Director of Hudbay Minerals Inc. (2010-2016), Senior Vice President, Finance and CFO and Director of Agnico- Eagle Mines Ltd. (1998-2010), and Treasurer of Inmet Mining Corp. (1990-1998). David was recognized as the Mining Person of the Year by the Northern Miner in 2012 and was named Canada’s CFO of the Year by Financial Executives International Canada in 2009. He holds a B.Comm with distinction from the University of Toronto, is a fellow of Chartered Professional Accountants (FCPA, FCA) and a Certified Director of the Institute of Corporate Directors (ICD.D). He is also a Director of the Greater Vancouver Board of Trade and the Vancouver Symphony Orchestra.

SUSTAINABILITY

At Interra, corporate governance is a critical factor to achieve sustainability with the important role to plan, implement and achieve business objectives, aligning management actions with stakeholders’ interests. Interra recognize the significance of a well-integrated environment, social and governance (ESG) strategy guided by the highest business procedures and ethics standards. Interra‘s Board and Team are inclusive, efficient, accountable, and equipped with diverse competences to nurture a long-term, proactive and safe approach with integrity, transparency and care for the environment, its people and its communities.

Interra‘s Sustainability Strategy rests on 3 pillars:

People

Interra is cognizant of its role as an Employer and its responsibility to shape an inclusive and diverse workforce, and as a Neighbor to maximize the opportunities and mitigate the risks of its presence, respecting the culture and rights of its communities.

Environment

Interra‘s environmental stewardship is guided by continuous improvement towards minimizing adverse impacts and ensuring its people cultivate the necessary awareness to follow or surpass environmental safety and regulatory guidelines set forth by governments and the industry to protect our ecosystems.

Governance Integrity

Interra believes that Corporate Governance takes more than just complying with laws and regulations as a pathway to fulfilling the objectives of its operations. It takes Good Governance, which implies the highest level of ethics and compliance, and more importantly, the comprehension that decisions have consequences. We aim to earn the trust, respect and support of our stakeholders by making decisions more inclusive and transparent.

Company Details

Interra Copper Corp.

Suite 1100 – 1111 Melville Street

Vancouver, BC, V6E 3V6 Canada

Phone: +1 604 283 9858

Email: Investors@InterraCopperCorp.com

www.InterraCopperCorp.com

Listing Date: September, 24, 2019

CUSIP: 46072A / ISIN: CA46072A2020

Shares Issued & Outstanding: 28,873,037

Canadian Symbol (CSE): IMCX

Current Price: $0.24 CAD (01/19/2024)

Market Capitalization: $7 Million CAD

German Symbol / WKN: 3MX/ A3DHGP

Current Price: €0.157 (01/19/2024)

Market Capitalization: €5 Million EUR

Contact:

www.rockstone-research.com

Disclaimer: This report contains forward-looking information or forward-looking statements (collectively "forward-looking information") within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: "believe", "expect", "anticipate", "intend", "estimate", "potentially" and similar expressions, or are those, which, by their nature, refer to future events. Rockstone Research, Interra Copper Corp. and Zimtu Capital Corp. caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Interra Copper Corp.´s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through its profile on SEDAR at www.sedarplus.ca. Please read the full disclaimer within the full research report as a PDF (see below and here) as fundamental risks and conflicts of interest exist. The author, Stephan Bogner, currently does not hold any equity position in Interra Copper Corp., however he owns equity in Zimtu Capital Corp., and is being paid by Zimtu Capital Corp. for the preparation, publication and distribution of this report, whereas Zimtu Capital Corp. holds an equity position in Interra Copper Corp. and will profit from volume and price appreciation Note that Interra Copper Corp. pays Zimtu Capital Corp. to provide this report and other investor awareness services. The cover picture and the picture with the house made of copper bricks have been obtained from DALL-E / OpenAI.

Disclaimer and Information on Forward Looking Statements: Rockstone Research, Zimtu Capital Corp. (“Zimtu“) and Interra Copper Corp. (“Interra“; the “Company”) caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Interra´s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through Interra‘s documents filed on SEDAR at www.sedarplus.ca. All statements in this report, other than statements of historical fact, should be considered forward-looking statements. Statements in this report that are forward looking include that there will be a copper fever heating up exploration; that Interra will grow its portfolio of copper projects; that a copper price rally to $15,000 USD/t is expected; that the threshold of $15,000 USD per ton seems to be the magic number for copper prices to inventivize new mine developments as supply is not keeping up with the strong demand growth; that copper is “on a necessary path to $15,000“ and “the most probable path for copper price from here – that both avoids depletion risk and as well as a sharp surplus swing – is to trend into the mid-teens by mid-decade; that copper prices need to double to $15,000 USD to spur new coppper supply; that copper prices could soar to $15,000 by next year; that such a dramatic price escalation could be akin to rocket fuel for pure-play copper exploration stocks; that Interra is strategically positioning its shareholders with direct exposure to the anticipated copper bull market; that Interra plans to advance its newly acquired Rip Project; that Interra also aims to further advance technical and exploration work at its other copper porphyry asset in British Columbia, the Thane Project; that you should consider: “Build your new house out of copper bricks, cover the copper with gypsum wallboard so you forget it’s in the walls. Ten years from now you’ll be able to tear down the house and buy a fleet of electric Lamborghinis with your profits.”; that the copper industry is facing a critical situation as the supply is dwindling while the demand remains high, possibly leading to dramatic future shortages; that a large number of copper mines are expected to stop production by 2035, which means that a substantial portion of the current supply will disappear in the next few years; that there is an impending copper supply-demand issue, and that all these factors lead to a problem in the copper market; that we‘re heading towards a supply-demand crunch; that only higher copper prices appear to be the solution to stimulate exploration and development of new copper supply; that the the current copper price is too low to incentivize new mines; that it is likely going to take a major out-of-stock event for the copper market to re-calibrate supply and demand with a price that both avoids depletion risk and a sharp surplus swing; that Goldman Sachs forecasted in 2021 that the copper price (in tonnes) will reach the mid-teens by mid-decade, and I’d say that’s on track, and that it may not be a gradual uptick but a sudden increase, and that will be an unpleasant surprise to end users; that looking ahead to 2024, market analysts anticipate a significant surge in copper prices, positioning this vibrant red metal to potentially surpass the performance of other commodities once more, and that this optimistic outlook acts as a powerful catalyst, fueling the momentum of stocks in the copper exploration sector; that copper could skyrocket over 75% to record highs by 2025; that copper is headed for a price spurt over the next two years, as mining supply disruptions coincide with higher demand for the metal; that rising demand driven by the green energy transition and a likely decline in the U.S. dollar in the second half of 2024 will push copper prices higher; that the investment bank forecast that the higher renewable energy targets would boost copper demand by extra 4.2 million tons by 2030, and that this would potentially push copper prices to $15,000 a ton in 2025; that other analysts see a bullish run for copper due to mining disruptions, with Goldman Sachs expecting a deficit of over half a million tons in 2024; that the winners of the copper rush will be mainly Chile and Peru; that that copper prices need to nearly double to $15,000 USD/t to prompt mining companies to build new mines to meet the rising demand; that if supply won‘t keep up with demand, copper prices could jump 10-fold; that when metals are required, the prices go crazy and nobody’s willing to sell them, and that we’re heading into that sort of situation; that results are pending from work at the Rip Project and that further exploration work is planned, consisting of geophysics to refine targets for the first stage of drilling; that work at Interra‘s Thane Copper Porphyry Project in British Columbia is also planned; that Interra will advance copper porphyry projects; that a revival of mining activities could be advantageous for neighboring companies like Interra; that Interra not only plans to explore the fully permitted Rip Project this year but also iholds ts 100% owned Thane Copper-Gold-Silver Porphyry Project; that Global demand for copper is expected to double by 2035; that as the world electrifies, urbanizes, and grows wealthier, demand for copper will be challenging to meet, potentially bolstering the price of the metal; that copper connects the past and future – generating exciting potential opportunities for investors; that demand for copper is forecast to grow from 25 million tons today to 53 million by 2050; that the electrification of transport is projected to have the largest impact on copper demand; that EV sales are projected to grow 35% in 2023; that copper demand from power grids is projected to grow nearly 5x by 2050; that the shift toward renewable power generation technologies such as solar and offshore wind should further increase demand; that the growing demand from building construction, appliances, electrical equipment, and cell phones, is still projected to account for 58% of copper usage by 2035; that by the early 2030s, demand could outstrip the current supply by more than 6 million tons per year; that global copper output is expected to peak by the mid-2020s; that 1.4 billion tonnes of new copper is needed to reach net zero by 2050; that over the next 27 years, the world will demand nearly twice the volumes of copper the world has produced over the last 3,000 years; that over 700 million metric tonnes of copper are required in the next 22 years alone; that in 2050, annual copper demand will be greater than all copper consumed from 1900-2022; that mine supply will fall well below demand by 2024. Such forward-looking statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. It is important to note that Interra‘s actual business outcomes and exploration results could differ materially from those in such forward-looking statements. Risks and uncertainties include that the option agreement with ArcWest may not be fulfilled by Interra and that the project returns to ArcWest; further permits may not be granted timely or at all; the mineral claims may prove to be unworthy of further expenditure; there may not be an economic mineral resource; certain exploration methods that were thought would be effective may not prove to be in practice or on the claims; economic, competitive, governmental, geopolitical, environmental and technological factors may affect Interra‘s operations, markets, products and prices; Interra‘s specific plans and timing drilling, field work and other plans may change; Interra may not have access to or be able to develop any minerals because of cost factors, type of terrain, or availability of equipment and technology; and Interra may also not raise sufficient funds to carry out or complete its plans. Additional risk factors are discussed in the section entitled “Risk Factors“ in Interra‘s Management Discussion and Analysis which is available under Core‘s SEDAR profile at www.sedarplus.ca. Further risks that could change or prevent these statements from coming to fruition include that Interra and/or its partner will not find adequate financing to proceed with its plans; that management members, directors or partners will leave the company; that the option agreement to acquire the properties will not be completed and that the properties return back to the vendors; that Interra will not fulfill its contractual obligations; there may be no or little geological or mineralization similarities between Interra‘s properties and other properties in Chile, Canada or elsewhere; that uneconomic mineralization will be encountered with sampling or drilling; that the targeted prospects can not be reached; that exploration programs, such as mapping, sampling or drilling will not be completed; that uneconomic mineralization will be encountered with drilling, if any at all; changing costs for exploration and other matters; increased capital costs; interpretations based on current data that may change with more detailed information; potential process methods and mineral recoveries assumption based on limited test work and by comparison to what are considered analogous deposits may prove with further test work not to be comparable; mineralization may be much less than anticipated or targeted; intended methods and planned procedures may not be feasible because of cost or other reasons; the availability of labour, equipment and markets for the products produced; world and local prices for metals and minerals; that advisory terms may be changed or no positive results from the advisory are reached; and even if there are considerable resources and assets on any of the mentioned companies‘ properties or on those under control of Interra, these may not be minable or operational profitably; the mineral claims may prove to be unworthy of further expenditure; there may not be an economic mineral resource; methods Interra thought would be effective may not prove to be in practice or on its claims; economic, competitive, governmental, environmental and technological factors may affect Interra‘s operations, markets, products and prices; Interra‘s specific plans and timing of them may change; Interra may not have access to or be able to develop any minerals because of cost factors, type of terrain, or availability of equipment and technology, or political landscapes; and Interra may also not raise sufficient funds to carry out its plans; nationalization of assets in Chile or elsewhere may occur, or other political laws and regulations may force Interra to leave the country or halt exploration and development at its projects. The writer assumes no responsibility to update or revise such information to reflect new events or circumstances, except as required by law. Cautionary Notes: Stated references of other companies or projects are not necessarily indicative of the potential of Interra and its properties in Chile and Canada, and should not be understood or interpreted to mean that similar results will be obtained from Interra. Results of stated past producers, active mines, exploration and development projects elsewhere are not necessarily indicative of the potential of Interra‘s projects and should not be understood or interpreted to mean that similar results will be obtained from Interra. A Qualified Person has not verified the mineral resources and reserves in the the resources and reserves from other deposits and companies which are presented in this report, which are for illustrative purposes only and are not necessarily indicative of the mineralization to be found on the properties held by Interra. The historical information on Interra‘s properties or near-by projects or elsewhere is relevant only as an indication that some mineralization occurs on Interra‘s properties, and no resources, reserve or estimate is inferred. A qualified person has not done sufficient work to classify the historical information as current mineral resources or mineral reserves; and neither Rockstone nor Interra is treating the historical information as current mineral resources or mineral reserves.

Disclosure of Interest and Advisory Cautions: Nothing in this report should be construed as a solicitation to buy or sell any securities mentioned. Rockstone, its owners and the author of this report are not registered broker-dealers or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer. Never make an investment based solely on what you read in an online or printed report, including Rockstone’s report, especially if the investment involves a small, thinly-traded company that isn’t well known. The author of this report, Stephan Bogner, is not a registered financial advisor and is paid by Zimtu Capital Corp. (“Zimtu”), a TSX Venture Exchange listed investment company. Part of the author’s responsibilities at Zimtu is to research and report on companies in which Zimtu has an investment or is being paid to conduct shareholder communications. So while the author of this report may not be paid directly by Interra Copper Corp. (“Interra”), the author’s employer Zimtu is being paid and will benefit from appreciation of Interra’s stock price. The author currently does not own equity of Interra, however he owns equity of Zimtu Capital Corp. and thus will also benefit from volume and price appreciation of its stock. Interra pays Zimtu to provide this report and other investor awareness services. As per news on March 10, 2023: Interra “entered into a number of agreements, each effective upon closing of the Transaction, for the provision of marketing and communications services and to build awareness of the Company with investors... Agreement with Zimtu Capital Corp. for a term of 12 months. The Company will pay a fee of $150,000 + GST.” Overall, multiple conflicts of interests exist. Therefore, the information provided should not be construed as a financial analysis but as an advertisement. The author’s views and opinions regarding the companies featured in reports are his own views and are based on information that he has researched independently and has received, which the author assumes to be reliable but may not be. Rockstone and the author of this report do not guarantee the accuracy, completeness, or usefulness of any content of this report, nor its fitness for any particular purpose. Lastly, the author does not guarantee that any of the companies mentioned will perform as expected, and any comparisons made to other companies may not be valid or come into effect. Please read the entire Disclaimer carefully. If you do not agree to all of the Disclaimer, do not access this website or any of its pages including this report in form of a PDF. By using this website and/or report, and whether or not you actually read the Disclaimer, you are deemed to have accepted it. Information provided is for entertainment and general in nature. The cover picture and the picture with the house made of copper bricks have been obtained from DALL-E / OpenAI. Data, tables, figures and pictures, if not labeled or hyperlinked otherwise, have been obtained from Interra Copper Corp., Stockwatch.com, Tradingview and the public domain.