Disseminated on behalf of Commerce Resources Corp. and Zimtu Capital Corp.

2022 is on its way to mark the historic year when some critical REEs (Rare Earth Elements) have slipped into a supply deficit, first and foremost neodymium (Nd) and praseodymium (Pr). Both these highly sought-after metals are needed to produce permanent magnets for electric vehicle motors and wind turbines, to name a few.

With demand expected to grow strongly, the NdPr supply deficit will be expanding to dramatic levels, reaching a shortfall in 2030 equal to 3 times the projected NdPr oxide output of the Mountain Pass REE Mine in California. As new large REE mines are needed to have a meaningful impact in reducing the supply deficit, the Ashram REE & Fluorspar Deposit in Quebec should come into mind as it matches up with some decisive characteristics in comparison to the only 2 major REE miners in the western world today: MP Materials Corp. from the United States and Lynas Rare Earths Ltd. with operations from Australia and Malaysia. “O Canada, we stand on guard for thee!“

With Commerce Resources Corp. having sent the first batch of mixed rare earth carbonate (REC) concentrate samples to global processors means that they are now in the process of figuring out:

1) If the mixed REC concentrate can be processed profitably into separated REE oxides with >99% purity, and

2) If the REC can be used to blend with REC concentrates from their other feedstock sources.

Based on the strong NdPr oxide distributions of these first mixed REC samples, it is already clear today that the Ashram REE & Fluorspar Deposit in Quebec compares very favourably to other active REE mines, including those in China. What makes Commerce Resources so attractive is the lookout to produce some 25,000 t of REO equivalent annually, which puts the company in the same neighbourhood as MP Materials and Lynas, both of which are building large separation plants in Texas.

Today, there are just two major REE miners in the western world, currently with similar market valuations:

MP Materials Corp. (NYSE: MP; market capitalization: $6.4 billion USD)

and

Lynas Rare Earths Ltd. (AEX: LYC; market capitalization: $8.8 billion AUD, or ~$6.1 billion USD at current FX rate)

For the last quarter (ending June 30, 2022), Lynas Rare Earths Ltd. recently announced sales revenue of $294.5 million AUD (~$207 million USD at current FX rate), whereas MP Materials Corp. recently announced revenue of $143 million USD for its second quarter of 2022.

Although composition and form of concentrate differ between both companies, the data still shows that there is a very high profit margin between selling a mineral concentrate (MP Materials) versus selling intermediate rare earth products such as NdPr oxide (Lynas).

Full size / Source: MP Materials Corp.’s news-release on August 4, 2022.

“MP Materials helps fuel the electrification of global infrastructure. We are the largest producer of rare earth materials in the Western Hemisphere, through our state-of-the-art, zero-discharge operations in Mountain Pass, California. We currently deliver approximately 15% of global rare earth supply with a long term focus on Neodymium-Praseodymium (NdPr), a crucial input to the powering of electric vehicles, wind turbines, drones, robots and many other advanced technologies.“ (Source:

MP Materials)

Full size / Source: Lynas Rare Earths Ltd.’s news-release on July 18, 2022.

“During the period, rare earth prices were sustained at recent high levels, especially the NdPr price which remained between 70% and 80% higher than at the same time last year. NdPr production of 1,579 tonnes and total REO production of 3,650 tonnes was achieved during the quarter. This was lower than in the third quarter due to ongoing and unpredictable water supply interruptions from our local supplier in Malaysia. “ (Source: Lynas Rare Earths)

Ryan Castilloux of Adamas Intelligence said he expects the current strong pricing environment for magnet rare earths to stay. “Notwithstanding the market’s typical ebbs and flows led by seasonality and other short-lived transient factors,” he added...Castilloux said the full extent of demand growth continues to be suppressed by auto industry microchip bottlenecks...“On the flip side, however, demand growth from the EV sector has continued to perform well, albeit it is also being tempered by cell and component shortages.” Overall, Adamas Intelligence is expecting global neodymium magnet demand to increase by 10 percent this year. The firm expects the so-called magnet rare earths to collectively see the strongest demand growth in H2...

The ore produced at Mount Weld is concentrated on-site into a mineral concentrate and is then shipped to the Lynas Advanced Materials Plant (LAMP) in Malaysia for processing into NdPr oxide plus several other ancillary products.

MP Materials must sell all of its mineral concentrate to processors in China, who separate it into individual REOs, as the company does not have a separation facility yet (expected to be operational in Texas in late 2022).

According to MP Materials: “Since restarting operations, MP Materials has overcome the operational challenges faced by the site’s previous owner and scaled production at Mountain Pass dramatically. In 2020, MP Materials produced more than 38,500mt of rare earths in concentrate [i.e. 38,500 t of REO equivalent in mineral concentrate form], representing more than 15% of global consumption and an all-time high in the 60-year history of Mountain Pass. The mixed rare earth [mineral concentrate] we produce today is an intermediate product that requires further processing in Asia. Following completion of our Stage II optimization project, expected in 2022, MP Materials will re-commission the integrated processing facilities at Mountain Pass. Concurrently, the MP Materials Stage III team is working to restore the capacity to manufacture rare earth metals and permanent magnets in the United States.“

Despite a high strip-ratio of 6:1 (waste-to-ore), MP Materials‘ production costs ($1,750 USD/REOt) are just a fraction (an eighth) of the average realized sales price ($13,918 USD/REOt). This shows that there is also a high profit margin to be made by just mining and selling a mineral concentrate, as being showcased by MP Materials since restarting operations at Mountain Pass in 2017.

In a potential mining scenario, Commerce could either sell a monazite mineral concentrate to processors of such material (e.g. EFR, China, Saskatchewan Research Council), or a mixed rare earth carbonate to facilities like Silmet, Lynas‘ LAMP, China, or MP Materials‘ pending facility in Texas, or Commerce Resources could do partial separations and sell NdPr oxide to metallization facilities (e.g. LCM, etc.). The point being, Ashram has the right mineralogy and a preferred NdPr distribution that makes all these options potentially viable.

To whom could Commerce sell its mixed rare earth carbonate concentrate? To any processor in the world, because this concentrate form is the most readily usable feedstock to the vast majority of separation facilities globally. Also, the high NdPr distribution of the Ashram mixed REC samples produced to date (21-24%) make Ashram feedstock very attractive compared to its peers, including those companies in active operation.

While MP Materials‘ Mountain Pass Deposit in California (USA) has a long history of REE mining (1952-2002, 2012-2015; 2017-today), Lynas‘ Mt Weld Deposit is the only new major REE mine coming online in the western world in the last 20 years (mining at Mt Weld began in 2011). And to be clear, the global market for the REEs has more than doubled in the last decade, and Lynas’ production is less than a third of this increased new demand.

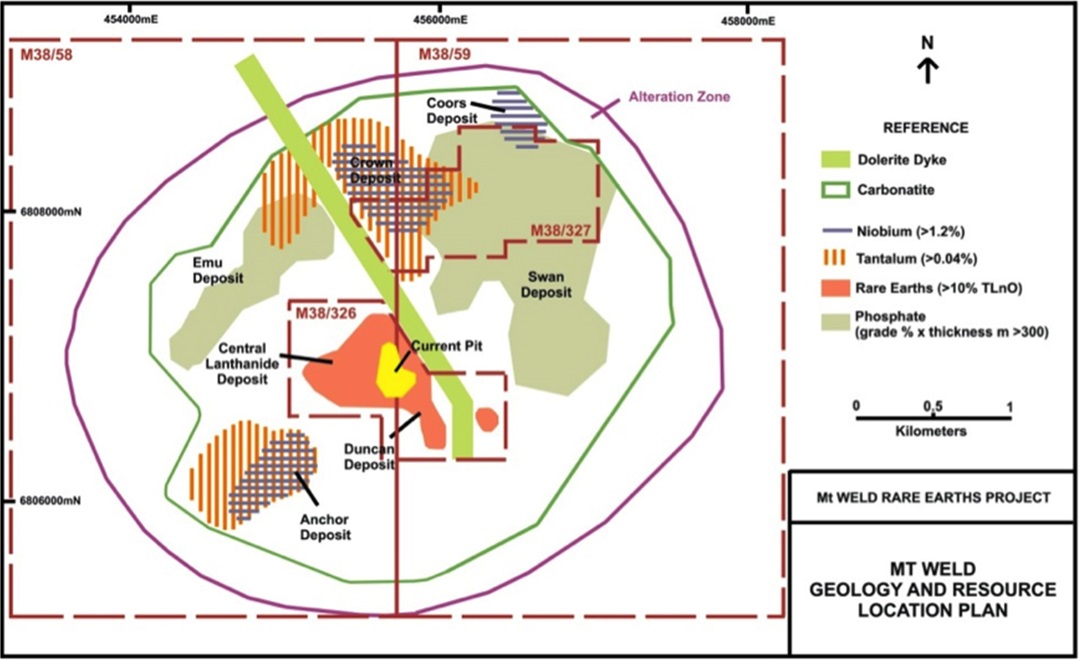

According to Lynas: “The Mt Weld Central Lanthanide Deposit (CLD) is one of the highest grade rare earth deposits in the world. Mt Weld also hosts the undeveloped Duncan (rare earth), Crown (niobium, tantalum, titanium, rare earths, zirconium) and Swan (phosphate) deposits. Lynas processes the CLD ore at the Mt Weld Concentration Plant to produce a rare earth [mineral] concentrate that is sent for further processing at Lynas Malaysia’s Advanced Material Plant near Kuantan, Malaysia.“

Full size / At Mt Weld, the highest concentration of rare earths is found in the Central Lanthanide Deposit (CLD) and is currently an open pit to a depth of 51 m. The carbonatite, which is approximately 3 km in diameter, also hosts a number of other deposits including the undeveloped Duncan, Crown and Swan deposits. (Source: Lynas)

Full size / “At Mountain Pass, the ultrapotassic rocks occur in seven larger stocks and as hundreds of small dikes... The principal economic mineral at the Project is bastnaesite, a rare earth fluorocarbonate with the generalized chemical formula LnCO3F... Bastnaesite mineralization at the Project is entirely restricted to carbonatite rocks and its nearby breccia... Mineralization occurs entirely within the Sulfide Queen carbonatite [highlighted in red above] within the Project area... The Sulfide Queen carbonatite, which hosts the mineralization at the Project is referred to as a stock but is a roughly tabular, sill-like body that strikes approximately north and dips to the west at about 40°... The largest single body is a composite shonkinite-syenite-granite stock approximately 6,400 ft [1,951 m] in length and 2,100 ft [640 m] wide (Olson et al, 1954)... The currently defined zone of rare earth mineralization exhibits a strike length of approximately 2,750 ft [838 m] in a north-northwest direction and extends for approximately 3,000 ft [914 m] downdip from surface. The true thickness of the >2.0% TREO zone ranges between 15 to 250 ft [4.6 to 76 m].” (Source: MP Materials Corp., 2021)

Full size / Cross-section (left) and oblique view (right) of the Ashram Rare Earth & Fluorspar Deposit’s principal mineralized zones. To be updated following completion of the 2022 drill program. (Source: Commerce Resources Corp., 2022)

With a total of 4.6 million t of contained REO, Lynas currently has almost twice as much REEs in the ground as MP Materials with ~2.5 million t of contained REO. With ~74 million t in combined reserves and resources (at grades between 5.4% and 8.4% TREO), Lynas currently sits on a larger tonnage deposit than MP Materials with ~41 million t @ ~6% TREO). In terms of contained REO, the Ashram Deposit is currently (2012) roughly in line with Lynas and has about 80% more REEs in the ground as MP Materials.

Both MP Materials‘ and Lynas‘ deposits are classified as very high-grade as most REE deposits globally host average grades between 0.1% and 4% TREO.

The Ashram Deposit hosts a Measured Resource of 1.6 million tonnes (Mt) at 1.77% rare earth oxide (REO) and 3.8% F, an Indicated Resource of 27.7 Mt at 1.90% REO and 2.9% F, and an Inferred Resource of 219.8 Mt at 1.88% REO and 2.2% F, at a cut-off grade of 1.25% REO. Mineral resources are not mineral reserves as they do not have demonstrated economic viability. There is no certainty that all or any part of the Mineral Resources will be converted into Mineral Reserves.

Mt Weld Reserves (Proved & Probable; June 2019):

19 million t @ 8.4% TREO

(containing ~1.6 million t REO)

Mt Weld Resources (Measured, Indicated, Inferred); June 2019):

55.2 million t @ 5.4% TREO

(containing ~3 million t REO)

Niobium Rich Rare Metals Project (Crown Deposit):

37.7 million t @ 1.07% Nb2O5

Mountain Pass Reserves (Proven & Probable; September 2021):

30.5 million t @ 6.36% TREO

(containing ~2 million t REO)

Mountain Pass Resources (September 2021):

Indicated: 1.4 million t @ 2.82% TREO

Inferred: 9.1 million t @ 5.1% TREO

The open pit that forms the basis of Mountain Pass‘ reserves and the LoM (life of mine) production schedule is approximately 3,100 ft from east to west [width: 945 m] and 3,800 ft from north to south [length: 1,148 m] with a maximum depth of 1,400 ft [depth: 427 m]. Total mining is estimated at 216 million st (short tons) comprised of 30.4 million st of ore and 186 million st of waste, resulting in a strip ratio of 6.1 (waste-to-ore).

Last week (August 12, 2022), Commerce Resources announced that the first two step-out holes of its 2022-drilling program have extended the mineralized footprint at the Ashram REE & Fluorspar Deposit in Quebec by an additional ~100 m to the southeast. Assays are pending, but based on the geological core logging of these two holes, the Ashram Deposit now has a mineralized footprint that now extends at least 700 m along strike (remains open), 300 m in width, and 600 m to depth (remains open).

“This further solidifies the monazite dominant Ashram Deposit as one of the largest rare earth element deposit’s globally,“ the company noted in its news-release and added the following: “Apart from one additional drill hole planned at the south end of the deposit to further improve confidence in the geological model, the remainder of the drill holes (~3-4 holes totalling ~1,100 m) will be focused on infill drilling with the objective of increasing resource confidence from the inferred/indicated categories to the indicated/measured categories in areas where the neodymium-praseodymium (“NdPr”) contents are highest.“

“Depending on the location within the deposit, the NdPr distribution – i.e. % of Nd+Pr oxide of the total rare earth oxide (“REO”) – typically varies from 21-24+% with monazite being the dominant carrier of the rare earth elements (“REEs”). The drill hole plan has been developed by the Company’s primary Prefeasibility Study consultant (BBA Inc.) and is targeting infill of a larger pit shell (~+50%) compared to what was considered in the Project’s 2012 Preliminary Economic Assessment. This larger pit shell is anticipated to underpin an initial mineral reserve estimate upon completion of the Prefeasibility Study for the Project.“

According to Commerce Resources: “The Ashram Deposit hosts a well-balanced rare earth distribution anchored in the magnet feed rare earths (Nd, Pr, Tb, and Dy) which have the strongest market fundamentals over the near, mid, and long-term. In addition, within the overall resource, there exists a zone of more intense NdPr enrichment, termed the ‘MHREO Zone’. This mineralized zone contains an REE distribution of approximately 24% combined NdPr (19% Nd, 5% Pr) with significant Dy (0.9%) and Tb (0.2%). This type of magnet feed enrichment is unique to Ashram and extends from surface comprising a significant amount of the deposit’s total resource.“

In the rare earth industry, a mixed rare earth carbonate (“REC”) concentrate is typically viewed as the initial marketable product in the REE value chain. A mixed REC is readily saleable as it is the most common feedstock to REE solvent-extraction facilities globally, which refine and separate the individual REEs into marketable products (oxides with >99% purity) to be disseminated throughout downstream value chains.

Full size / Basket Price Comparison between Lynas’ Mt Weld Deposits, MP Materials’ Mountain Pass Deposit and Commerce Resources’ Ashram Deposit, showing that the 4 REEs used as Magnet Feed (NdPrTbDy) account for more than 90% of the value of all the REEs and that Ashram MHREO hosts the highest Magnet Feed distribution with 24.69% (Mountain Pass: 16%; CLD: 23.63%).

The REEs currently in highest demand are used as “Magnet Feed“ (i.e. for the manufacturing of magnets): Neodymium (Nd) and Praseodymium (Pd), Terbium (Tb) and Dysprosium (Dy).

Investors looking at a REE exploration, development or mining project focus on how these Magnet Feed REEs are distributed within the deposit.

The left part of above table shows that a REE deposit typically hosts the 15 rare earth elements (REEs) at different “distributions“:

The more Nd (in relation to other REEs) the better!

With 18.56% Nd distribution, “Ashram MHREO“ (the higher grade part of the deposit which could be mined before enlarging the open-pit to include the “Ashram Main“ zone) has a higher Nd distribution than Mountain Pass (12%) and Lynas (CLD: 18.13%, Duncan: 17.89%).

Material from Ashram MHREO is superior to both Lynas and MP Materials in terms of the percentage of the 4 REEs used in magnet manufacturing – Magnet Feed (NdPrTbDy): Commerce Resources has up to 24.69% of these, whereas MP Materials has just over 16% and Lynas up to 24.17%.

The right part of the table shows the USD-value of each deposit‘s REE distribution at current market prices (August 11, 2022):

The “Basket Price“ comparison of Magnet Feed REEs shows that rock from Ashram MHREO currently has a 72% higher value ($34.95 USD per kg of mixed REO) than Mountain Pass ($20.29 USD/kg) and a 18% higher value than Lynas‘ currently mined CLD Deposit ($29.69 USD/kg), with only Lynas‘ undeveloped Duncan Deposit fetching a slightly (2.5%) higher value ($35.82 USD/kg).

92% of the REO value in Ashram MHREO comes from the 4 Magnet Feed REEs (Pr, Nd, Tb and Dy). Roughly 2/3rd (72%) of this value comes from Nd (57%) and Pr (15%).

However, this is “just“ the basket price, a theoretical value of all the REEs within the rock, not accounting for any processing and assumming 100% recovery of each. In reality, only 4 of these REEs carry the bulk of the value in an REE deposit – Nd, Pr, Nd, and Pr, termed the Magnet Feed REEs.

On July 15, 2022, Commerce Resources announced to have completed “its first shipment of a mixed rare earth carbonate (“mixed REC”) concentrate sample to a major global producer of rare earth elements (“REEs”) for evaluation. The sample (gram quantities) meets typical market specifications and was produced as part of the Company’s ongoing scale-up to larger kilogram quantities.“

The company was “pleased to report the new sample has a neodymium (Nd) plus praseodymium (Pr) distribution – i.e. % of Nd+Pr oxide of the total rare earth oxide (“REO”) – of 24.2%, which is significantly higher than that reported by several major global producers, and that of the previous samples produced (21.6% and 22.4% NdPr).“ The company added that this “strong NdPr distributions that characterize these Ashram samples rank among the highest in the world for non-cerium depleted mixed REC concentrate and exceeds that of several major global producers. These samples were produced with the Company’s conventional flowsheet developed at Hazen Research, CO, in which several process operations have been demonstrated at a continuous pilot-scale level. The Company is now undergoing a process scale-up to kilogram quantities of mixed REC concentrate to deliver to additional third-party processors per their request.“

Most recently on July 22, Commerce Resources announced to have delivered “an initial shipment of 2 kg of Ashram Deposit whole rock crushed material to an emerging rare earth element (“REE”) processor per their request. This follows on the heels of the recently delivered sample of mixed rare earth carbonate (“mixed REC”) concentrate to satisfy the request of a major global producer... The 2 kg sample of Ashram Deposit whole rock crushed material will be used by the REE processor to assess processing at their internal laboratories and is expected to be followed in the near-term by an additional 200 kg shipment of crushed whole rock. The processor has also expressed interest in receiving a sample of mixed REC concentrate,“ and added:

“The Company continues to receive a marked increase in industry interest regarding providing samples for third party evaluation following the announcement that it had produced on-spec mixed REC from Ashram Deposit material (see news release dated March 23, 2022). This interest includes samples of unprocessed whole rock, high-grade monazite concentrate (>40% REO), and high NdPr mixed REC concentrate produced from the Ashram Rare Earth and Fluorspar Deposit. The Company is working diligently to provide samples to satisfy all third-party requests and is well advanced in its Ashram Project component studies which will culminate in a Prefeasibility Study on the Ashram Project targeted for the first half of 2023.“

Moreover, Commerce Resources‘ Ashram is not only one of the largest REE deposits in the world but also one of the largest fluorspar deposits. The company aims to include this valuable and critical mineral (fluorspar) as a by-product in its Pre-Feasibility Study (ongoing), whereas neither MP Materials nor Lynas currently produces any by-products apart from REEs (though Lynas sits on large undeveloped niobium, tantalum and phosphate deposits; similar to Commerce Resources with its niobium-project-optioneer Saville Resources Corp.).

“For nearly 50 years, carbonatites have been the primary source of niobium and rare earth elements (REEs), in particular the light REEs, including La, Ce, Pr, and Nd. Carbonatites are a relatively rare type of igneous rock composed of greater than 50 vol % primary carbonate minerals, primarily calcite and/or dolomite, and contain the highest concentrations of REEs of any igneous rocks. Although there are more than 500 known carbonatites in the world, currently only four are being mined for REEs: the Bayan Obo, Maoniuping, and Dalucao deposits in China, and the Mountain Pass deposit in California, United States. The carbonatite-derived laterite deposit at Mount Weld in Western Australia is also a REE producer. In addition to REEs, carbonatite-related deposits are the primary source of Nb [niobium], with the Araxá deposit, a carbonatite-derived laterite in Minas Gerais state, Brazil, being the dominant producer. Other commodities produced from carbonatite-related deposits include phosphates, iron, fluorite, copper, vanadium, titanium, uranium, and calcite.” (Source).

“It makes no sense for America to extol our own environmental enlightenment while outsourcing the vast majority of our mining to places without environmental protections, yet that’s what we’ve been doing for decades, and we’re still doing it today. Something has to change. “We can keep talking till the cows come home,” said Althaus. “It’s time for action.”” (Source: Forbes, May 2022).

“Electric car sales doubled in 2021 to a new record of 6.6 million, as per the International Energy Agency. And while EVs accounted for less than 8 percent of global sales last year, and just under 10 percent in Q1 2022, projections from consultant AlixPartners show they could reach 33 percent globally by 2028 and 54 percent by 2035.” (Source)

Company Details

Commerce Resources Corp.

#1450 - 789 West Pender Street

Vancouver, BC, Canada V6C 1H2

Phone: +1 604 484 2700

Email: cgrove@commerceresources.com

www.commerceresources.com

Shares Issued & Outstanding: 91,654,630

Canada Symbol (TSX.V): CCE

Current Price: $0.155 CAD (08/18/2022)

Market Capitalization: $14 Million CAD

Germany Symbol / WKN (Tradegate): D7H0 / A2PQKV

Current Price: €0.117 EUR (08/18/2022)

Market Capitalization: €11 Million EUR

Previous Coverage

Report #35 “Major Step Forward: Commerce Resources succeeds in producing marketable mixed rare earth carbonate sample“

Report #34 “All Roads Lead To Ashram, Eventually“

Report #33 “Research & Advisory Firm looks into the Ashram REE & Fluorspar Project from Commerce Resources“

Report #32 “Already Big Ashram Gets Bigger And Bigger“

Report #31 “Fluorspar: The Sweet Spot for Quebec‘s Steel and Aluminium Industries“

Report #30 “Lean and Mean: A Fighting Machine“

Report #29 “Like A Phoenix From The Ashes“

Report #28 “SENKAKU 2: Total Embargo“

Report #27 “Technological Breakthrough in the Niobium-Tantalum Space“

Report #26 “Win-Win Situation to Develop One of the Most Attractive Niobium Prospects in North America“

Report #25 “The Good Times are Back in the Rare Earths Space“

Report #24 “Commerce Resources and Ucore Rare Metals: The Beginning of a Beautiful Friendship?“

Report #23 “Edging China out of Rare Earth Dominance via Quebec‘s Ashram Rare Earth Deposit“

Report #22 “Security of REE Supply and an Unstoppable Paradigm Shift in the Western World“

Report #21 “Commerce well positioned for robust REE demand growth going forward“

Report #20 “Commerce records highest niobium mineralized sample to date at Miranna“

Report #19 “Carbonatites: The Cornerstones of the Rare Earth Space“

Report #18 “REE Boom 2.0 in the making?“

Report #17 “Quebec Government starts working with Commerce“

Report #16 “Glencore to trade with Commerce Resources“

Report #15 “First Come First Serve“

Report #14 “Q&A Session About My Most Recent Article Shedding Light onto the REE Playing Field“

Report #13 “Shedding Light onto the Rare Earth Playing Field“

Report #12 “Key Milestone Achieved from Ashram’s Pilot Plant Operations“

Report #11 “Rumble in the REE Jungle: Molycorp vs. Commerce Resources – The Mountain Pass Bubble and the Ashram Advantage“

Report #10 “Interview with Darren L. Smith and Chris Grove while the Graveyard of REE Projects Gets Crowded“

Report #9 “The REE Basket Price Deception & the Clarity of OPEX“

Report #8 “A Fundamental Economic Factor in the Rare Earth Space: ACID“

Report #7 “The Rare Earth Mine-to-Market Strategy & the Underlying Motives“

Report #6 “What Does the REE Market Urgently Need? (Besides Economic Sense)“

Report #5 “Putting in Last Pieces Brings Fortunate Surprises“

Report #4 “Ashram – The Next Battle in the REE Space between China & ROW?“

Report #3 “Rare Earth Deposits: A Simple Means of Comparative Evaluation“

Report #2 “Knocking Out Misleading Statements in the Rare Earth Space“

Report #1 “The Knock-Out Criteria for Rare Earth Element Deposits: Cutting the Wheat from the Chaff“

Contact:

Rockstone Research

Stephan Bogner (Dipl. Kfm.)

8260 Stein am Rhein, Switzerland

Phone: +41-44-5862323

Email: info@rockstone-research.com

www.rockstone-research.com

Commerce Resources Disclaimer: Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. Forward Looking Statements: This news release contains forward-looking statements, which includes any information about activities, events or developments that the Company believes, expects or anticipates will or may occur in the future. Forward looking statements in this news release include that we expect to complete a prefeasibility study for the Ashram Project; that mixed REC is readily saleable; that partial separation will allow for a marketable neodymium and praseodymium oxide to be produced; that we may move downstream early in the mine-life through partial separation; that Ashram has the potential to become one of the largest fluorspar deposit and a long-term supplier to the met-spar and acid-spar markets; and that the Company is positioning to be one of the lowest cost rare earth element producers globally. These forward-looking statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. Risks that could change or prevent these events, activities or developments from coming to fruition include: that we may not be able to fully finance any additional exploration on the Ashram Project; that even if we are able raise capital, costs for exploration activities may increase such that we may not have sufficient funds to pay for such exploration or processing activities; the timing and content of any future work programs; geological interpretations based on drilling that may change with more detailed information; potential process methods and mineral recoveries assumptions based on limited test work and by comparison to what are considered analogous deposits that, with further test work, may not be comparable; testing of our process may not prove successful or samples derived from the Ashram Project may not yield positive results, and even if such tests are successful or initial sample results are positive, the economic and other outcomes may not be as expected; the availability of labour and equipment to undertake future exploration work and testing activities; geopolitical risks which may result in market and economic instability; and despite the current expected viability of the Ashram Project, conditions changing such that even if metals or minerals are discovered on the Ashram Project, the project may not be commercially viable; The forward-looking statements contained in this news release are made as of the date hereof and the Company assumes no responsibility to update or revise such information to reflect new events or circumstances, except as required by law.

Rockstone Disclaimer: This report contains forward-looking information or forward-looking statements (collectively "forward-looking information") within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: "believe", "expect", "anticipate", "intend", "estimate", "potentially" and similar expressions, or are those, which, by their nature, refer to future events. Rockstone Research, Commerce Resources Corp. and Zimtu Capital Corp. caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Commerce Resources Corp.´s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through their respective profiles on SEDAR at www.sedar.com. Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist. The author, Stephan Bogner, holds a long position in Commerce Resources Corp. and Zimtu Capital Corp., and is being paid by Zimtu Capital Corp., which company also holds a long position in Commerce Resources Corp. Note that Commerce Resources Corp. pay Zimtu Capital Corp. to provide this report and other investor awareness services. The cover picture (amended) has been licenced and obtained from Roman_studio.